This was posted at the Speakeasy on March 4, 2016, and is being reposted here by request. :D

Hello Wimms,

You obviously have a good understanding of how GLD works from a technical standpoint. But I can tell from your comment that you do not have a very good understanding of what I have been explaining.

First of all, in characterizing your perception of what I've been explaining, you used the following words and phrases: "quite a bit of monkey business"; "conspiring"; "shady business"; "to cheat"; "fraudulent"; and "assuming conspiracy". But nothing in my "coat check view" is any of those things. None of it is illegal, fraudulent, or in the least bit shady. I meant it, and I still mean it, what I wrote in one of my comments to Maus69: "No conspiracy. No plan. Nothing illegal about it. It’s just the correct way to understand GLD and how it works."

There are plenty of gold bugs (even here at the Speakeasy) who want to believe that GLD is in some way fraudulent. But I am not one of them. Often they read what I write about GLD and interpret it through their own "GLD-is-fraudulent lens", and then post a comment that reveals that lens. So I want to say it again here, as plainly as possible, that I do not think there's anything illegal or fraudulent about GLD, even under the coat-check room view. For anyone who thinks it is "shady business" that the physical in GLD will ultimately go to someone other than the shareholders of GLD, all I can say is you didn't read the small print. Or if you did, then you didn't understand it the correct way, which is what I'm explaining.

I can tell by your comment, Wimms, that I need to go back and explain "coat check" from the beginning. And to do so, I will also need to explain "bullion banking" from the beginning. Understanding bullion banking is the key to everything, and I'm starting to think that not even one in a million gold bugs (and even gold and investment industry professionals) actually understands what bullion banking is. Bullion banking didn't even exist before 1971. Back then, it was just called banking. And it's no coincidence that the establishment of the LBMA by the Bank of England in 1987, as an umbrella association for the London Bullion Market, coincided with the birth of "this new gold market" that Another described. Such an association was necessary for bullion banking to function in "this new gold market."

Before I do, however, I want to address a couple of things from your comment. The first is that you really seem to take issue with my characterizing transactions in layman terms. I do this not only because it makes it easier to understand, but also because it helps to get across the correct way to view what is actually happening.

The main example here is that you didn't like when I wrote that GLD "buys" gold from HSBC. Here's exactly what I wrote:

"From GLD’s perspective, it “buys” and “sells” its gold outright. But it always “buys” from HSBC, and it always “sells” to HSBC. So like Maus69 says, GLD always owns its gold outright, but HSBC holds it for GLD."

Then you wrote:

"Now lets focus on assumptions you presented as facts.

First, GLD trust does not buy or sell anything, not from HSBC, nor any of the APs."

There's a reason I wrote it the way I did, and I think it will be helpful to explain why. First of all, notice that I put "buy" and "sell" in quotation marks. In a previous paragraph, I wrote (more precisely) that, "HSBC might lease gold from someone else to increase its reserves, and then it might allocate some of its reserves to GLD." Allocate is the key word there. "Buy" in quotes meant allocate, and "sell" in quotes meant "unallocate" or "deallocate."

So why did I write "buy" and "sell" rather than allocate? Because it gets us closer to understanding what's really happening. No matter where the physical gold bars come from initially, they all come from HSBC's reserves right before they "go into" GLD. Even if an occasional numbered bar added to the list is physically somewhere other than HSBC's own vault (and I doubt this is ever the case, but it is possible), it must be allocated to HSBC and become part of HSBC's pool of physical reserves before it is placed on the bar list.

Part of HSBC's job as custodian is to identify specific bars by their numbers. And when they are going "into" or "out of" GLD, they are doing so "from" or "to" HSBC's pool of physical reserves (quotes in this sentence are used because the movements are often just on paper, and the physical metal doesn't actually move). The transaction is not explained this way or using these words in the prospectus or the Participant Agreement, but my version actually explains more clearly what is meant in the official documents.

I highlighted a relevant line from the Participant Agreement you linked:

3. DEPOSITS

3.1 PROCEDURE: You may at any time notify us of your intention to deposit Precious Metal in your Unallocated Account. A deposit may be made (in the manner and accompanied by such documentation as we may require) only by transfer from an account of yours relating to the same kind of Precious Metal and having the same denomination as that to which this Unallocated Account relates. We will not accept physical delivery of Precious Metal into this account.

They are talking about an AP making a deposit into the Trust's account at HSBC. What do you think it means that they will not accept physical delivery into that account? It means allocated, or bar numbers. It means, in essence, that deposits from APs do not include bar numbers. Bar numbers come only from the custodian.

This will make more sense once I explain bullion banking the way you've probably never heard it explained before, but in order for HSBC to assign a bar to the Trust, it must first be or become one of HSBC's own bars, meaning one of its physical reserves. This bar, as a reserve of HSBC, is an asset of HSBC which gets transferred to "The Trust" when it gets allocated to the GLD bar list. It is no longer an HSBC asset once it is on the GLD bar list. In essence, GLD "bought" that bar from HSBC.

So what did HSBC receive in exchange for surrendering one of its assets to "The Trust"? It received payment from the Trust's unallocated account in exchange for one of its reserves. Now, that account is also at HSBC, so the unallocated credits in the Trust's account are actually HSBC liabilities. So, in a sense, it is more like a withdrawal by the Trust. But then again, remember that HSBC continues holding the bars on behalf of the Trust, so that's why it's called allocation.

I also used "buy" and "sell" to make the point that GLD owns it outright. This is important because the entity owning it outright has the exchange rate exposure, which GLD wants and needs. If, hypothetically, gold bar numbers could be leased by GLD directly (a contention that came up in the comments which I was indirectly addressing with that paragraph), then GLD would not have the exchange rate (price) exposure to the gold, because in a lease, the price at which gold will be returned is agreed in advance as part of the lease. You have to own it outright (not borrow it) to profit (or lose) from its price movements. I believe this "outright ownership" was made a little more clear using "buy" and "sell" rather than saying HSBC "allocated" some of its unallocated physical to GLD.

This concept also affects HSBC in the case that it did lease some physical gold. Forget about the lease having anything to do with GLD share creations, which was something else that really seemed to bother you. If HSBC leased some physical gold bars from anyone, it does not have price exposure, meaning it does not gain if the price of gold rises, and it does not lose if the price of gold falls. Yet those bars still become the "free and clear" assets of the bank. It just also has a new liability to provide gold to the lessor in the future at a set price, which neutralizes any gain or loss from the price of gold during the lease.

Now let's say that HSBC allocates some bars to GLD, while it still has that outstanding lease. By doing this, HSBC has taken on price risk, which it now must hedge, because it still has to return some gold to the lessor at a predetermined price, but it has reduced its reserves, de-neutralizing that liability. This is what I was talking about here:

"But I can imagine an AP, today, preferring to pass the buck and make HSBC source the gold and hedge its subsequent exposure (if the gold is leased), rather than expanding its own balance sheet and having its own delta-one desk hedge off the risk."

Wimms, you objected to the idea that HSBC might lease physical to fulfill its duty as Custodian. You wrote:

"you say that HSBC can create GLD shares with gold it does not own title to. This is not true."

The way you put it is not what I say. If HSBC leases gold bars from a client, it can sell them or let them be withdrawn, or allocate them to someone else. For all intents and purposes, HSBC has perfectly clear title to those bars, even though they were leased. That's because HSBC is not only a bank, it is a bullion bank.

An apt analogy, whether you like it or not, is physical cash at your neighborhood bank. If your bank has borrowed some cash because it was running low, it can put that borrowed cash into its ATM machine where you may withdraw it. So yes, HSBC can create GLD shares with gold bars it has leased from someone else. That someone else holds, as an asset, a liability from HSBC, and the physical bars are absorbed into the bank's pool of reserves, becoming assets of the bank, on par with any other assets of the bank, as far as what the bank can do with them.

So, in essence, HSBC may borrow some bullion banking reserves (physical gold bars), and then "The Trust" may make a "withdrawal" from its unallocated account, essentially pulling out those same reserves that were borrowed and sticking them into GLD. GLD now owns them outright. It doesn't matter that HSBC leased them a few days prior, because gold is fungible, and because HSBC is a bank, and because of something very special that sets banks apart from non-banks, which is the ability to hold deposits as on-balance sheet assets of the bank.

Bullion Banking 101

Imagine you're the CEO of a small asset management firm. That won't be a stretch for several of you who I know have your own firms. What is the most fundamental difference between your firm and a bank? Yes, banks create money and you can't do that, but there's something even more fundamental than that, something that enables banks to create new money. Can you think of what it is?

Remember Jon Corzine and MF Global? MF Global went bankrupt in 2011. And Jon Corzine, its CEO, faced possible criminal charges in the bankruptcy, but why? Many companies go bankrupt. Going bankrupt is not against the law, so how did MF Global break the law?

Here's an excerpt from the MF Global Wikipedia page:

"MF Global mixed customer funds and used them for its own account for at least several days before the bankruptcy and transferred funds outside the country.[27]

The liquidation trustee ultimately reported that on October 26, 2011, Edith O’Brien, an assistant treasurer in Chicago who reported to the firm’s treasurer in New York approved transfers totaling $615 million from segregated customer trust accounts at JPMorgan Chase, supposedly for an intraday loan. The funds weren’t returned by the end of the day, causing “panic” in Ms. O’Brien’s operation. Ms. O’Brien continued to approve such “loans” in the ensuing days.

On the morning of October 28, two company officials noted a deficit in segregated customer accounts of about $300 million. Two members of O’Brien’s staff improperly determined that a $540 million wire transfer into the segregated accounts the previous day had somehow gone unrecorded and double-counted the transfer. The firm reported a surplus of more than $200 million to the commodities commission. The segregation report was revised to show a surplus without any backup documentation.

That same day, the 28th, CEO Jon Corzine ordered O’Brien to transfer $175 million to JPMorgan to cover a firm overdraft. With no other source for the cash, O’Brien approved a transfer of $200 million from a customer trust account at JPMorgan. The trustee’s report concludes there was a substantial “shortfall” in customer segregated funds every day from Oct. 26, when $615 million in loans from customer accounts were not repaid, until MF Global filed for bankruptcy on Oct. 31.

[…]

U.S. regulators subpoenaed MF Global’s auditor, PricewaterhouseCoopers LLP, for information on the segregation of assets belonging to clients trading on U.S. commodity exchanges.[54]

[…]

Bloomberg reported that "Barry Zubrow, JPMorgan's chief risk officer, called Corzine to seek assurances that the funds belonged to MF Global and not customers. JPMorgan drafted a letter to be signed by [Edith] O'Brien to ensure that MF Global was complying with rules requiring customers’ collateral to be segregated. The letter was not returned to JPMorgan."[63] Corzine resigned from the firm in early November 2011.

[…]

On April 24, 2012, Jill Sommers, a CFTC commissioner, outlined possible enforcement actions against MF Global employees and executives. Potential violations involve rules that require segregation of customer funds from a brokerage's own operating accounts…"

Here's a quote from the GLD prospectus which I used in the last post. The only thing I did here was replace "Custodian" and "bullion dealer" with HSBC, the name of the bank acting as both in some if not most cases:

Gold held in an unallocated account is not segregated from HSBC's assets. The account holder therefore has no ownership interest in any specific bars of gold that HSBC holds or owns. The account holder is an unsecured creditor of HSBC…

It's not a perfect analogy, the difference of which I'll get to in a moment, but I am making a point here about HSBC being a bank, while MF Global and your own small asset management firm are not. In London, it's called the Client Money Rules:

CASS 7.13 Segregation of client money

Application and purpose

CASS 7.13.1G01/06/2015

The segregation of client money from a firm's own money is an important safeguard for its protection.

CASS 7.13.2R01/06/2015

Where a firm establishes one or more sub-pools, the provisions of CASS 7.13 (Segregation of client money) shall be read as applying separately to the firm's general pool and each sub-pool in line with CASS 7.19.3 R and CASS 7.19.12 R.

Depositing client money

CASS 7.13.3R01/06/2015

A firm, on receiving any client money, must promptly place this money into one or more accounts opened with any of the following:

(1)

a central bank;

(2)

a CRD credit institution;

(3)

a bank authorised in a third country;

(4)

a qualifying money market fund.

(Source)

Banks are exempt from the Client Money Rules:

Depositaries

CASS 1.4.6R01/01/2009

The client money chapter does not apply to a depositary when acting as such.

(Source)

Here's a short excerpt from a paper on this subject:

"It follows then that what enables banks to create credit and hence money is their exemption from the Client Money Rules. Thanks to this exemption they are allowed to keep customer deposits on their own balance sheet. This means that depositors who deposit their money with a bank are no longer the legal owners of this money. Instead, they are just one of the general creditors of the bank whom it owes money to.

[…]

What makes banks unique and explains the combination of lending and deposit-taking under one roof is the more fundamental fact that they do not have to segregate client accounts, and thus are able to engage in an exercise of ‘re-labelling’ and mixing different liabilities, specifically by re-assigning their accounts payable liabilities incurred when entering into loan agreements, to another category of liability called ‘customer deposits’.

What distinguishes banks from non-banks is their ability to create credit and money through lending, which is accomplished by booking what actually are accounts payable liabilities as imaginary customer deposits, and this is in turn made possible by a particular regulation that renders banks unique: their exemption from the Client Money Rules."

(Source)

Here's my question again. Can you answer it now? "Imagine you're the CEO of a small asset management firm. What is the most fundamental difference between your firm and a bank? Yes, banks create money and you can't do that, but there's something even more fundamental than that, something that enables banks to create new money. Can you think of what it is?"

Okay, I said above that this was not a perfect analogy, and what I meant is that bullion banking is not precisely similar to regular banking where you need a banking license and have a central bank. It is more similar to eurodollar banking, or carrying bank-like books in a foreign currency, or even in something else, like a wealth asset.

Keep imagining you have your own asset management firm, and let's say you're inside the US. If you wanted to carry bank-like books in dollars, you'd need to get a banking license to do so. But if you (hypothetically) did so in a foreign currency or gold, there's no such banking license to even be issued. You'd be theoretically acting outside of the purview of that currency's banking authority, and without the safety net of a lender of last resort. The eurodollar system is a good example. This is from What the World Needs Now:

“And just to be sure we’re on the same page, the eurodollar is not to be in any way confused with the euro, but rather stands to mean the artificial supply of “U.S. dollars” that “exist” as accounting units in off-shore banks, having originally been authentic deposits of New York’s finest export, but which were then subsequently lent on – fractionalized and derivatized into a vast amorphous mass as only a network of cooperating banks can do best. ”

[…]

“Think about Eurodollars. Think about European banks outside of the Federal Reserve System making dollar denominated loans or simply issuing dollar liabilities to FX traders. Sure they have a few physical dollars in reserve. But they don’t have direct access to the Fed lending facilities. So if they find themselves short on reserves, they will have to go into the market to buy some dollars, just as you say. Which, in aggregate, could drive up the price of the dollar versus the euro.”

This is what banks do. It is how they "create money". They create an artificial supply of something by being able to take deposits, lend them out, and keep it all on their own balance sheet.

Say you want to be a rock bank. So you take a deposit of 10 rocks from your neighbor Steve, and you lend those 10 rocks to your other neighbor Gary, who deposits them at your rock bank of course. You now have two deposits of 10 rocks each on the liability side of your balance sheet, and on the asset side you have a promissory note from Gary as an asset worth 10 rocks, plus your 10 rock reserves. But Gary might choose to withdraw 9 of his rocks from his account, and then you'll be down to 11 rocks deposited, but only 1 physical rock in your reserves. So, with that withdrawal, your reserve ratio dropped from 50% (10 physical rock assets held against 20 rock liabilities) to 9% (1 physical rock asset against 11 rock liabilities). See how it works being a bank? And notice, also, that your reserve ratio is out of your control.

That's basically what bullion banks do. They create an artificial supply of gold on their balance sheet. Wimms asked:

"Where does the idea come from that all of London unallocated gold is fractional reserve? Unallocated account only means that you do not have specific bars attached. Whether it is fractionally reserved or fully reserved is completely separate matter and depends on the contract with BB."

The answer is, we know it because they are banks… bullion banks, and that's what banks do. Jeff Christian, who has been working with bullion banks since the 80s, says they are fractionally reserved just like banks. The LBMA is a banking system, not unlike the Federal Reserve System is a banking system, so you can't really say this part is fractionally reserved and that part is not. The system itself is fractionally reserved. Their own survey of daily turnover amounts to more gold changing hands each day (2,700 tonnes) than is mined in an entire year. The LBMA was asked if the numbers in the survey included FOREX trading of XAU/USD, etc.., and they said yes it does. And Anthony Fell of LBMA bullion bank and GLD AP, RBC, said, "At Royal Bank of Canada, we trade gold bullion off our foreign exchange desks rather than our commodity desks, because that’s what it is – a global currency."

We tend to think of bullion banking like this:

When it's really more like this:

Here are just a few of the LBMA bullion banks that don't even have LBMA-approved gold vaults, yet still keep books denominated in gold ounces: BNP Paribas, CIBC, Citibank, Commerzbank SA, Credit Agricole, Credit Suisse, Goldman Sachs, Morgan Stanley, RBC, Société Générale, Standard Bank and Standard Chartered Bank, and that's not even half of them. Many of these banks are actually LBMA market makers, and even GLD APs, and none of them even touch the metal.

Here's a snip from The View: A Classic Bank Run:

"To clarify the distinction for our readers, let us consider a bullion bank with a physical ounce asset backing an unallocated ounce liability to its clients. If that bullion bank then lends that physical to a jewellery company who use it in their operations, then the bullion bank now has an ounce claim asset backing its unallocated ounce liability. From your point they are short “physical” but I would also note that the bullion bank is not short “financially”, that is they are not exposed to any movement in the price of gold."

This is what I meant in my last post when I said that the huge stock of paper gold in existence constitutes a short position by the banks:

"Yes, the LBMA has huge daily turnover. That’s the flow, and it implies an enormous “stock” of spot unallocated gold credits sitting on the aggregate LBMA books. Please understand that this “stock” is essentially a gigantic short position."

It's a short position in the same sense that your neighborhood bank is short physical dollars. Your bank only has a tiny proportion of physical dollars on hand relative to the amount of customer deposits it has. In fact, if you want to make a large withdrawal in cash, you have to give the bank a few days' notice.

It's a short position that would become a big problem in a bank run situation if it was still 1930, but today your neighborhood bank has an ace in the hole. That ace is that the central bank can, in a pinch, print an unlimited amount of reserves.

Here's another excerpt from The View: A Classic Bank Run. I can tell you now that the email from "a friend" (the parts in blue) was from Aristotle:

It is important to start thinking of these gold operators as the banks that they are, because then you can start to see the significance of the CBs publicly announcing, through the twice-renewed CBGA, that they are no longer going to be the lender of last resort to this system. Quote: "The signatories to this agreement have agreed not to expand their gold leasings…" You cannot be a backstop without expanding!

Furthermore, you will be able to see how the very act of commercial banking (which is lending) automatically creates a ginormous synthetic supply of whatever the system's reserves are. Think credit money versus cash, or even M3 versus M0 once you throw in a few derivatives. The LBMA today clears 18,000,000 ounces, or 560 tonnes of paper gold liabilities every single day. That's down from its peak of 1,359 tonnes in December, 1997 when Another started writing. That's each and every day! It's all right here.

And that's just the part the LBMA clears. A Friend writes:

"A bank can be "populated" with unallocated gold accounts in two primary ways. It can either be done as a physical deposit by a silly person or by another corporate entity, or else it can occur completely in the non-physical realm as a cashflow event whereby a customer with a surplus account of forex calls up and requests to exchange some or all of it for gold units, whereupon the bank acts as a broker/dealer to cover the deal – occurring and residing on the books as an accounting event among counterparties rather than as any sort of physical purchase. No bread, no breadcrumbs, only a paper trail and metal of the mind. This is how the LBMA can report its mere subset of clearing volumes averaging in the neighborhood of 18 million ounces PER DAY. Just a whole lot of "unallocated gold" digital activity as an ongoing counterparty-squaring exercise."

Here is an analogy that my Friend wrote me in an email:

"It is here that I offer the eurodollar market as a very good parallel to the bullion sector of banking. While not a perfect parallel (for all the most obvious reasons) it provides a remarkably good bridge to help anyone who has a good footing on modern commercial banking to successfully cross over to that seemingly unfamiliar territory of "bullion banking". In fact, they need do little more to successfully cross over than to simply think of bullion banking ops as though they were eurodollar banking ops – the difference being that whereas eurodollar banking makes extra-sovereign use of the U.S. dollar as its accounting basis in international banking activities (thus outflanking New York's purview and restrictions), bullion banking engages in similar "extra-sovereign" use of gold ounces within its operational/accounting basis (thus outflanking and overrunning Mother Earth's domain and tangible restrictions)."

That's what I'm trying to do here, to bridge your thought process from banking to bullion banking. I think everyone (or virtually everyone) thinks about bullion banking and the LBMA as being similar to the rest of the non-bank gold industry, when, in reality, it is much more similar to the commercial banking industry than the physical gold industry.

If you read that GLD Participant Agreement with your gold industry hat on, or even just your standard thinking hat, it reads just like Wimms portrayed the procedures. There's "gold this" and "precious metal that," and "bullion whatnot" all throughout, all of which reads like it involves physical moving around but doesn't. That's because we are imagining physical moving around when we read those sentences, but with our banking hats on, we can see that it's simply like saying "dollars must be tendered," or "it's a cash account," or "money was deposited," or "how much currency," none of which necessarily means physical cash.

The LBMA was created in 1987, in part as a direct result of the collapse of bullion banking pioneer, Johnson Matthey Bankers, in 1984. From Seventeen:

"It was a mess that had to be cleaned up by the Bank of England itself, and in the aftermath, the BOE assumed the supervisory role over the London bullion market and demanded that the participants create a formal body to represent them as a group. A little more than a year later, in Dec. 1987, the LBMA was born."

It was around this same time that, as FOA explained, "a new gold market was being created was when bullion banks were allowed to sell Central Bank gold "ownership invoices", for cash to the benefit of Barrick." And later in that same post, "It wasn't long before gold was lent without any gold at all! No different than "fractional reserve" banking."

The rest of FOA's post is in this video, for those of you who need a break: ;D

Notice that I haven't even mentioned GLD yet. That's because, so far, I'm just trying to pound it in that the LBMA is a banking system, an association of banks. Bullion banking didn't exist before 1971. Back then it was simply called banking because, back then, gold was monetary reserves in the banking system. Bullion banking is, by definition, fractional reserve banking, and keep in mind that the LBMA is a natural carryover from the old gold standard. And most important to bear in mind, is that physical gold is the "physical cash" in the LBMA banking system. When we say "gold this" and "gold that," it's like saying "dollars this" and "dollars that," and the word "gold" within the LBMA means physical gold about as much as the word "dollars" means physical cash.

I said the dollar banks have an ace in the hole, which is that the CB can create an unlimited amount of cash if necessary. Obviously you can't do that with physical gold, but the bullion banks have an ace in the hole too. That ace is cash settlement.

Coat Check 101

First of all, I didn't come up with the idea of GLD being viewed as a central coat-check room for the bullion banks. I got it from Randy Strauss in 2011, and the earliest reference I've seen was in 2004, right after GLD was launched. By the way, the $POG had already risen 70% from 2001 to the launch of GLD in 2004, and I don't agree with Wimms' theory about GLD pulling the suppressing demand away from futures and thereby supporting the rising $POG. It was a commodity bull market, simple as that.

In mid-2010, we can see from the chart below that phase 1 ended. And in early 2011, the GLD inventory started to drop. The big drop (green arrow) was on January 25th, a big 31 tonne puke, and my Who is Draining GLD? post was four days later. That's when the coat check room idea first crossed my radar, and when it first appeared on my blog.

The price of gold was also dropping, from $1,400 at the beginning of 2011, to $1,324 on the day of the puke. And there were numerous stories in the MSM about the outflow from GLD being symptomatic of the souring of investor sentiment toward gold. That's when Randy Strauss wrote two posts about GLD that really caught my eye. The first one was on Jan. 14th, and the second one was on the 25th, the day of the puke:

RS View: Silly reporters. Instead of calling these “outflows” from the ETFs, it should be called what it is — a redemption of a basket of shares for physical gold by the Authorized Participants (e.g. bullion banks). Such share redemptions would actually be a bullish sign because it entails a reduction in the global supply of paper gold while at the same time signifying a preference by the redeeming party for having the metal over the ETF shares. That is, of course, unless the drawdown in physical gold merely represented the routine sales of the gold inventory that occur to cover the ETF’s administrative expenses.

RS View: I’ve said it before and I’ll say it again now, the reporters are getting it wrong when they equate outflows of gold from the ETFs with “sour” investor sentiment. What they need to work harder to understand is that these are NOT actively managed funds whose gold inventory is tweaked to ebb and flow based on public sentiment in the shares. Instead, the ETFs are more like a central coat-check room in which the various bullion banks have temporarily hung out their own inventories (i.e., meaning, their unallocated stock which they hold loosely on behalf of their depositors). And whereas the claim tickets (ETF shares) may freely circulate on the open market, any significant outflow of physical inventory is simply and primarily indicative of a bullion bank reclaiming the original inventory based on a heightened need or desire for physical metal in a tightening market — for example, to meet the demands emerging from Asia.

I was emailing with Randy at the time, and he explained a lot more about GLD to me than was in his posts. I also happened to be "IMing" (this was 2011, back when AOL Instant Messenger was still in use) with one of my readers at the time, a fellow I dubbed "Small Giant" in the post. He was an investment industry professional and long-time gold bug, so I was surprised to learn that he knew nothing about GLD redemptions, baskets, Authorized Participants, all the stuff I was learning from Randy. All that stuff, the stuff that everyone seems to know at least something about today (perhaps because that post got more than 50,000 views) was the focus of the post. Coat check wasn't even a footnote. In fact, it only appeared in the post once, and that was in Randy's quote above.

Soon, however, GLD inventory mechanisms became old news, while the sentiment-related creation/redemption myths continued. They did evolve, however, from being related to gold sentiment in general, to being related to investor sentiment toward GLD specifically, relative to gold sentiment in general. And they still persist to this day. Even Wimms' comment repeats the myth, more or less. From his comment:

"When there is a spike of GLD share selloff, orders are matched with buyers or APs as DTC market makers buy the shares themselves. So after a peak of selloff APs would own lots of GLD shares. They can sit on them as a buffer, or they can chose to redeem them. There is no requirement by GLD to sell the phys gold off. GLD the trust does not care. Trust only cares about one thing - that there is gold pledged for every basket of shares they have created, and they charge for every basket holding, so there is cost attached to sitting on the parked GLD shares to APs. That gives incentive to redeem when too many baskets are redeemable. Whether they sell off that gold on the market or not is of no interest to GLD trust.

When there is a peak of buying and GLD runs out of "free" (AP owned) shares, the price of GLD tries to go above market and there lies profit, so there is incentive for APs to create a basket and have shares to sell. For that they need to source gold and they are in business. It's not a physical arb at all. It's just the way GLD trust works. They have the right to sell shorts into DTC. This allows to handle sudden spikes of GLD buying as sourcing gold and basket creation is a slow process. Later when they have created a basket, they can cancel shorts. That may be happening all the time and we just do not see it due to low reporting frequency.

It is this part of the process that is interpreted as physical arb that is making the GLD to track spot price. It is not of course. But it can be presented as phys arb in a loose sense. If, and only if noone else is buying/selling in the open market, and if, and only if APs always sell/buy each basket's worth of gold on the open market, then GLD would have some impact on the spot price. But thats not what GLD is for. Its purpose is exactly opposite - to NOT have any impact on physical price.

So of course GLD market makers are using paper deals to track spot price. They run HFT on the DTC shares and set the spread and capture orders that don't have a counterparty. When there are no share transactions, they do nothing. They don't need to do anything for GLD to track the spot price. The price of gold backing the GLD shares is moving by itself together with spot, and market makers simply adjust their spread reference price along with it. Market makers are effectively doing the mark to market of the GLD gold reserves on the continuous basis."

This specific discussion, about why GLD's inventory changes, gets right to the crux of "coat check". Read it again, paying attention to why he says pukes and chugs happen. He says that redemptions (pukes) happen because of "a spike of GLD share selloff". And creations (chugs, like are happening right now) happen because of "a peak of buying".

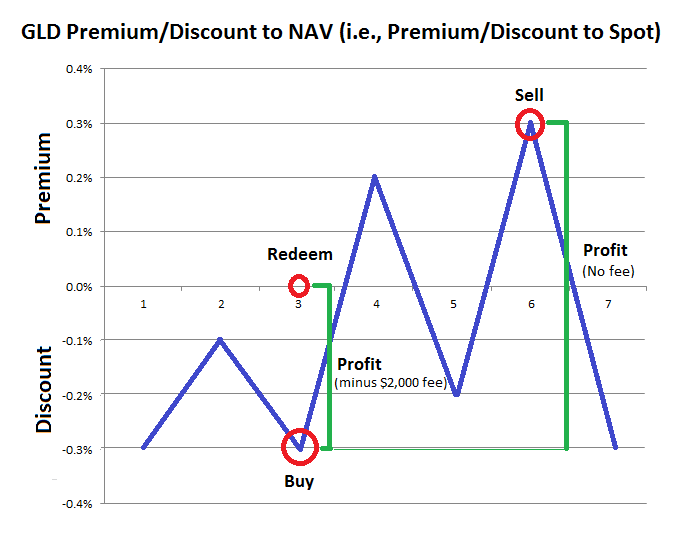

He objects to calling it a "physical arb" which is fine with me. Let's simply call it "sentiment-driven inventory changes." That's not saying it's required by the trust, but he says it simply happens because the APs end up with a lot of shares, and find it cheaper to redeem them than to sit on them. But why not sell them instead? Why are sitting on them or redeeming them the primary options? In fact, they aren't. I made the point in my last post, and even made a conceptual chart illustrating the point, that there is greater profit in selling shares captured by the arb than in redeeming:

It may seem like splitting hairs, but this really is the continental divide of the entire debate, whether gold is being "pulled" into and "pushed" out of GLD by "investor sentiment", or whether inventory changes are ultimately, primarily and fundamentally a free choice of the bullion banks, which essentially makes GLD a "reserve management" tool of the LBMA. You may bury your head in the sand and tell yourself it's a bit of both if it makes your brain hurt thinking about it, but logic dictates that it is primarily and fundamentally one or the other, and the implications of each are as vast as a drop of rainwater flowing to the Pacific if it lands on one side of the hair, and to the Atlantic if it lands on the other.

I think it is obviously the latter, that pukes and chugs are fundamentally a choice of the bullion banks, and GLD is essentially a reserve management tool of the LBMA, even though it doesn't specify that in the prospectus. I think this is the correct way to view GLD, and I think that using the correct lens reveals things that other people can't see. And I think that what we're now calling "sentiment-driven inventory changes" are simply (and obviously, to me) a myth, albeit a persistent and widely-accepted one.

For me this is intuitive, but that doesn't mean it's based on faith. After five years of thinking about, discussing and debating the subject, I have consciously reasoned that which is also intuitive. And now I will attempt to enumerate the ways in which the "coat check view" makes sense, while the "sentiment-driven view" does not.

Let's start with Wimms' description above. If I may summarize it in a single paragraph, the APs "help" GLD track the price of gold through HFT (high frequency trading run by computers and algorithms), and when there's a spike in selling (negative sentiment), the APs' HFT algorithms capture more shares than normal. At some point, they find it most efficient to redeem these shares rather than to hold them, because GLD charges a small storage fee. When there's a spike in buying (positive sentiment), the APs' HFT algorithm are allowed to essentially sell short (to sell shares that don't yet exist), racking up a larger short position than normal. And at some point, they find it most efficient to buy some physical and pledge it to GLD in order to unwind their short position, because, well, he doesn't really give us a reason, but I read it as that's something the Trust expects them to do in exchange for being allowed to sell short during positive sentiment spikes.

I'm going to break this down as quickly as possible, so try to keep up with me. ;D

The first issue is whether the APs are obliged to do this (to "help" GLD track the price of gold), or if they want to do it because they make a profit doing it. Pretty much everyone on both sides of the debate agrees it is done voluntarily, for profit. That was an easy one, but I needed to mention it.

Now, because this arbitrage is being done for profit, we can safely assume it's not just one AP doing it, it's several, and also that other non-AP HFT players might be doing it as well. And with competitive arbitrageurs in play, there will be plenty of liquidity and therefore no reason for any one arb to accumulate an overly-large position. So I'll ask it again. Why would the HFT algos not close out their position by selling the shares once the selling pressure has abated? It's a rhetorical question, because they have every reason, from more profit to less work and less cost, to sell those shares rather than redeem them. And if they are redeeming but not selling the redeemed gold as Wimms proposed (because of GLD's storage fees), then it's a bet not an arb, because they are not squaring their position, and that makes no sense under the "sentiment-driven view". Not to mention that most of these APs would have storage costs on physical reserves anyway, because they aren't LBMA custodians.

Now let's talk about creations, since that's what's happening right now. There are two relevant spreadsheets which anyone can download from the GLD website, the daily spreadsheet of historical data, and the bar list. The creation procedure takes three days from purchase order to bar allocation, and the bar list is three days behind the daily spreadsheet. Today (Thursday, 3/3/16), the bar list is showing 777 tonnes in the Trust's allocated account, which was the total on Monday, three days ago, and the daily spreadsheet is showing 793 tonnes which is the current total.

So far this year, we've had 42 trading days, and during that time, 150.96 tonnes have been added to GLD. Out of the 42 days, there were 14 days (a third of the time) with no change to the inventory. There were 3 days (7% of the time) with net redemptions. And there were 25 days (60% of the time) with additions, i.e., net creations. So on average, that's a little over 6 tonnes on each day some was added, but actually, there were two days with more than 19 tonnes per day added, and three more days with 12, 14 and 15 tonnes added. It's those five days I want to look at a little more closely. And there's one more day I'll include, December 18th, the day the rise started, with 18.74 tonnes added that day.

One thing the daily spread sheet reports as well as the inventory is the daily trading volume in shares. When GLD started in 2004, each share was worth 0.1 ounces, or 1/10th of an ounce. But the way that the Trust pays itself its fees is by slowly decreasing the weight of each share, so today, the shares are each worth 0.09561 ounces. I will use this weight to convert the daily share volume to tonnes, so we can see what percentage of the trading would have to be sentiment-related on those days, and then we can decide if that even passes the sniff test. ;D

So here are the dates in question, the daily volume in tonnes, the net-creations in tonnes, and finally the percentage of volume used to create new shares (under the "sentiment-driven view):

In case you're thinking we should also take the previous day's trading volume into account, in case there's a hangover effect happening, two of the previous days had lower trading volume, and three had higher (remember that two of the chug days were consecutive). In fact, the two lower trading days were so much lower that all of the preceding days were, on average, 12.6% lower volume than the chug days.

So, for the slow, this little exercise means that, if Wimms is right, then the spike in buying was almost 50% of the volume on those days, yet volume didn't jump nearly that much. Volume even declined a little on three of the days. So it could just be that 50% of the sellers disappeared, so the APs had to "naked" short 49% of the volume, and then put on some clothes by buying 98.45 tonnes of physical gold metal (the sum total of those six chugs). That's 98 pallets, or 7,913 LGD bars, in six days. Does that pass your sniff test?

On the other hand, I like the way those numbers fit with my current theory of short term hedge fund bets on the price of gold, as big as up to half the daily trading volume, so that the only way they made sense was OTC or off-market, i.e., creating new shares. Two more things in my view make this theory even more plausible. Normally these bullion banks would simply take the other side of that bet themselves, but according to my view, LBMA reserves are tight, most if not all of them are already in GLD and/or HSBC's vault, so the bullion banks are trying to reduce their bullion books right now, not increase them. And these banks do not have to find someone to sell them those 7,913 400-oz. bars. They simply have to transfer the hedge fund's cash to HSBC or another approved LBMA gold dealer, request an exchange into gold credits, and transfer the gold credits into the Trust's unallocated account at HSBC.

If Wimms is right, then I'm totally wrong about that, and so was Ari when he wrote this:

"A bank can be “populated” with unallocated gold accounts in two primary ways. It can either be done as a physical deposit by a silly person or by another corporate entity, or else it can occur completely in the non-physical realm as a cashflow event whereby a customer with a surplus account of forex calls up and requests to exchange some or all of it for gold units, whereupon the bank acts as a broker/dealer to cover the deal – occurring and residing on the books as an accounting event among counterparties rather than as any sort of physical purchase. No bread, no breadcrumbs, only a paper trail and metal of the mind."

Forget about how or where HSBC came up with those bar numbers. Without that element of the story, and with only the APs creating new shares for the hedge funds to bet big on gold without moving the market, and then wiring the hedge funds' money to London, to fund a FOREX account, and then exchange USD for XAU to transfer to HSBC and fund the creations… does that not pass the sniff test? And this is just a theory, unlike my c-c view which is fact. ;D

In his new email today (the first one), Wimms paraphrased the "Creation Process" from the AP Agreement:

3. AP notifies Custodian it will deliver gold to its unallocated account on day 2 (it could be physical tango, or deallocation)

The highlighted part is not in the document. It is Wimms editorializing, and he missed one option. It could be physical tango, deallocation, or, as Ari called it, "a cashflow event… No bread, no breadcrumbs, only a paper trail and metal of the mind."

8. Trustee creates and issues shares to AP. Note that this happens NOT before 3rd business day after initial AP request is filed.

The actual shares are created and credited to the AP's account at the DTC on the 3rd day, after allocation, but they show up on the daily spreadsheet on the first day. We know this because, as I pointed out earlier, the bar list is three days behind the daily spreadsheet.

Why is this important? Because it shows the order and importance of events. The actual, real shares being issued and listed at the DTC is basically a mere technicality that happens after the fact, not before. As far as the market is concerned, the new shares are out there, in someone's account, and possibly being traded, at least three days before "real" shares technically exist (if they came about the way Wimms says, through an AP shorting operation). Let's call this the "leeway" afforded to APs. Or maybe that's not the best term. It's essentially a temporal separation, a disconnect, between the technical aspects of creation/redemption that happen between the AP, the Trust and the Custodian, and what happens in the market between the AP and its clients. There is this potential disconnect of a few days between the two, and it works in the other direction too.

With creations, as Wimms pointed out, the AP may short sell shares and then put in a Purchase Order with the Trust after the fact. Likewise, it may have agreed to create shares for an OTC client, like Hedge Fund X, and then put in the Purchase Order after the fact. The Trust doesn't care about the details that led up to the Purchase Order, it only cares about how many baskets the AP wants to create.

So in the other direction, with redemptions, it follows that the Trust doesn't know or care about the details between the AP and its clients that led up to the redemption, it only cares about how many baskets are to be redeemed. Therefore, it follows that an AP can request redemption before the fact. That is, before buying the shares back "from the market." And if that AP is HSBC, the bars could theoretically be out the door and on their way to Switzerland before it buys back the shares. It can, of course, only redeem as many shares as it owns per the DTC at the time of redemption, but it can always buy more from another AP if it needs more.

Further on, Wimms says:

"You may also notice that the whole process of creation and redemption is by design at least 3 days long. This creates incentive for AP to have sufficient number of baskets on hands to handle 3 days worth of trading volume. This pretty much makes phys arb impossible, and requires forward thinking. Thus, if AP is anticipating high volatility, they may preemptively start creation of baskets."

While technically correct, this is wrong because it makes it seem like the AP is at the mercy of future volatility, i.e., investor sentiment. It makes it seem like the AP is essentially forced by the GLD market to create or redeem shares. This is the wrong view. It is always a choice.

The three-day process makes practical sense, plain and simple, and I never saw it like Wimms characterizes it, as a means "to counter BB questionable behaviour when GLD was created." That's pure rubbish as far as I'm concerned.

HSBC, being an AP and the custodian for the Trust, has a lot of leeway simply by the fact that a good portion of that three-day process was allotted for communication between AP and Custodian, and the time needed for bar identification. I wouldn't even be surprised if HSBC occasionally had bars, say, already loaded on the forklift, before they had technically been deallocated from the Trust. And I wouldn't even consider that questionable behavior. It's within the rules.

Wimms writes:

"After rereading what FOFOA has said I think I better understand now what bothers me.

The way he presented a Fund could use GLD. That really doesn't click with me. Why? The basis of this maneuver is that it is cheap and fast for the Fund to get into GLD through forex purchase of gold credits.

It isn't fast. Now lets think about cheap for a moment. By selling to anyone XAU at spot, BB is taking the risk of spot movements and risk of buyer requesting delivery. Thats a large cost risk. Why would they do that? If it were so cheap to get into gold credits and cash out later, why isn't it used widely to get exposure to gold price movements? And if it is then 1) why go any further and into GLD and 2) how does BB hedge itself against speculators using unallocated gold to buy/hold/sell/profit as BB would be effectively the creditor of that profit?

If they hedge by buying spot with delivery from someone else on LBMA then this would move the market. If they buy from themselves, there is no hedge."

First, I must repeat that this Hedge Fund X explanation is just a theory, and therefore not critical to my coat-check room view. But yes, it is cheap and easy to get into gold credits and cash out later, and it is widely used to get exposure to the gold price. It's precisely what the LBMA does. The LBMA is the largest OTC gold market in the world, and it also runs XAU currency trading, which is a cheap, easy and quick way to get exposure to gold.

The GLD share creation process may take three days, but the bank facilitating the deal can give its client exposure to the $POG immediately, either directly, or by buying unallocated from another bank like HSBC. It's what banks do. It's why they have quants and delta-one desks, to hedge risk and price exposure through fancy derivatives made from correlated commodities and currencies. It's what I called expanding their bullion books, which I'm guessing they're trying to do the opposite right now. So, in this scenario, as soon as the GLD shares are created three days later, they can unwind the hedge and shrink their books back down to where they were.

"There is a difference between BB clients who deposits their owned physical LGD bar to BB vault and expect phys to be redeemable, and someone who uses cash to buy gold credits onto their unallocated account, isn't it? That difference cannot be totally ignored by BB, they need to cover up their asses."

There is a difference! You see it, I see it, and that's kind of the whole point of understanding bullion banking, because that's precisely what they do. They act like there is no difference. Not out of malice or anything like that, it's just what banks do. Let's go back to the physical cash analogy.

There is a difference between bank customers who deposit their owned physical cash and expect to be able to get cash out of the ATM later, and someone who wires foreign currency-denominated electronic credits, requests a currency exchange, and then expects to be able to withdraw cash later, isn't there? That difference cannot be totally ignored by the banking system, can it? They need to cover their asses, don't they?

No! That's what banks do! And in this case, it's what bullion banks do with gold!

I wrote about precisely this concept, that bullion banks do not differentiate their liabilities based on the type of deposit, way back in 2011, in Via Email:

"The daily LBMA clearing turnover has dropped to 18 million ounces today. But even at today's lower amount, if the 3 to 5 estimate above holds, it is still likely to be more than global ANNUAL gold mine production that is traded (OTC) every single day. And what do you think is actually being traded as if it were simply another foreign currency?

Bullion Bank liabilities! BBs make money like any other bank, on their ability to issue "liabilities" as if they were real money, willy-nilly.

How many of these "BB liabilities" are outstanding at any given point in the 24 hr. cycle? And do you think these liabilities have any LESS of a claim on the BB physical reserves (unallocated gold) than any other? The answer is that all BB liabilities have an EQUAL claim. Whether you deposited 2 tonnes of physical yourself 30 years ago after your rich grandfather died, or if you called in a currency exchange order last night. Equal ability to demand allocation."

Wimms again:

"I do not see the point of parking gold into GLD when there is no demand by the GLD buyers. Slack could be used to support GLD, but imo only to the extent that needs to be done to satisfy market demand for GLD shares. Thus I don't think that phase 1 was initiated by parking excess gold into GLD in exchange for dormant shares."

Who said there was no demand? There was plenty of demand, it just wasn't the driving force. And since there was plenty of demand, they weren't just "dormant shares."

Okay, I can see that I need to wrap this up and post it today, since Wimms is now fielding questions and comments from the peanut gallery, and if I don't wrap it up, I'll quickly drown in comments that need to be addressed. So what I'm going to do is to use a few "freehand analogies" to try and help you see how I view LBMA reserves, how the bars in GLD are a part of those reserves, and how draining GLD provides "cash for withdrawals". I think if you can simply see GLD the way I see it, all the other little details will make more sense. So I'll try to describe the picture rather than to continue enumerating details that are apparently hard to swallow for some of you.

I don't expect to convince Wimms. I never convinced Bron, and I think part of the reason is because he's in the non-bank gold industry. But hopefully I can at least clarify my view, since I think it was mischaracterized in Wimms' initial post.

I'm going to make a few statements here that will probably seem shocking and hard to swallow to some of you, but hopefully they'll make more sense in a few minutes.

Bullion banks do not want physical gold. They will buy it if someone approaches them to sell some, because they are market makers, but they don't go looking for it. That's because physical (or allocated) gold is "reserves" to them, and just like in regular banking, reserves are a dead asset. Just like a regular bank, they try to minimize the amount of cash/reserves they are holding. And, like a regular bank, they prefer to hold live assets with a yield over dead assets with no yield. And, in fact, physical gold is even worse than cash in that regard, because gold has more storage costs associated with it, so physical gold reserves actually have a negative yield.

Not all gold ETFs are equal. Eric Sprott, for example, had to go out and buy the gold to put in his ETF. I even had a reader who was involved in the creation of a new gold ETF back in 2011, who told me all about the process. The launch was canceled after the $POG crashed in September, but the plan was to create a fund like Sprott's PHYS, only with kilo bars being the minimum redemption rather than 400 oz. bars.

They didn't have the money to just buy all the gold outright, up front, so they had to source institutional investors on one side, and source the physical gold from the mints on the other. The idea was, you get institutional investors to pledge to buy X amount of shares, you source the amount of gold required to back X amount of shares, and then you essentially use the investors' money to buy the gold and launch the fund which will then trade on a public exchange. The reason behind creating this new ETF was not that there was all this extra gold that needed to go somewhere, nor was it all this demand for a new gold ETF. The reason was the money that can be made from the fees you get for running a gold ETF!

So Sprott and this kilo ETF that never happened, had to go out and buy the gold to back their shares. But GLD is the gold ETF of a bunch of LBMA bullion banks (yes, almost all of the APs are also bullion banks), so their gold came straight out of their reserves. Because even if a bullion bank buys some physical gold from a customer who wants to sell, it goes right into the bank's reserves. Bullion banks, practically by definition, have more outstanding gold liabilities than they have physical gold assets (reserves), so even if a bullion bank segregated some physical on its balance sheet, it would still be de facto reserves.

So as these bullion banks were essentially "selling" (there's that word again) their reserves to the new GLD ETF during phase 1, and receiving shares as payment which they then sold to customers for dollars, they were essentially allocating (there's that other word I was earlier using interchangeably with "selling" in quotes) reserves that were already offset by other gold liabilities. In other words, to quote Randy Strauss again, it was "like a central coat-check room in which the various bullion banks temporarily hung out their own inventories (i.e., meaning, their unallocated stock which they hold loosely on behalf of their depositors). And whereas the claim tickets (ETF shares) freely circulated on the open market, any significant outflow of physical inventory is simply and primarily indicative of a bullion bank reclaiming the original inventory based on a heightened need or desire for physical metal in a tightening market — for example, to meet the demands emerging from Asia."

For anyone still having trouble with the concept of "inventories held loosely on behalf of their depositors," let's try a couple analogies. First, imagine you are going to start your own business, a store. Let's say it's going to be a small, local hardware store. You're going to carry everything from nuts and bolts to John Deere riding lawnmowers. You don't have enough money to buy everything you're going to carry, but that's okay, because your suppliers will give you credit. They'll gladly place their particular items in your store, and you just pay them when someone buys their item.

See? You have all this valuable stuff in your possession, but you're really just the middleman in the flow of this stuff from its producer to its end user. In the meantime, it sits in your store. Your store is like a pool or an eddy in the stream-like flow of these goods from producer to end user. Your inventory is like the slack in the flow. Of course no one has come up with a hardware ETF yet, so that's about as far as I can take that analogy.

So now let's picture a different kind of business. Imagine you own a gold coin and bar fabrication business. You take raw gold bars and loose gold shot you get from the refineries, and you melt it down and make it into fancy investment-grade bars and coins, some of which you sell in your own fancy showroom, some you sell on the internet, and some you sell to other dealers, wholesalers and distributors.

Again, you don't have enough money to buy outright all the gold that is on your physical premises at any given moment in time, so you rely on credit from others. You must essentially finance your inventory, one way or another. At first you do it similarly to the hardware store owner. You pay the refineries, essentially, net-30, or net-60, or however long it takes to fabricate and sell your products. So as the refinery gives you some raw gold, you also take on a liability, kind of like a bank.

Over time, your business grows, and before you know it, you have 20 tonnes of gold, in various states of completion, on your premises at any given point in time. So let's say you decide to start selling "unallocated gold credits" for a "fully reserved gold pool" which you'll keep stored in your secure warehouse. For each "credit" you sell, you pull a piece of gold out of your slack in the flow, and set it aside. And each "credit" is always fully backed with physical in your warehouse. To prove it, anyone can come in and redeem their "credits" for gold coins any time they want. And when they do, they become just like any of your other end user customers.

Depending on how carefully you manage it, you could theoretically sell "credits" for up to 20 tonnes, your entire inventory. Think about it. At $1,260 an ounce, that's $810 million you could invest in Australian MBS, or something with an equally good yield!

What you've essentially done there is inventory finance. Only you've essentially double-financed your inventory. It's not a problem, though, as long as you never let your inventory drop below 20 tonnes, and that might mean turning down some orders from regular customers. Then again, it's unlikely that all of your "credit" holders will ever want to redeem at the same time, and you don't want to be turning down sales, especially if you have what they want in your warehouse. So you might start to let it drop below 20 tonnes from time to time, hedging off your price exposure elsewhere.

Congratulations, you have now become a bullion bank, or something similar, and this probably won't be a problem as long as there's not a run on your "cash in the ATM". And as a bullion bank, you will probably run your reserves down to a small fraction of your liabilities. But you've still got tonnes of gold just sitting there in your warehouse. Surely that’s a dead asset you can make a little more live. How about launching an Exchange Traded Fund, fully backed by the gold in your warehouse?

These shares won't be as redeemable by the public as your unallocated credits, but there will always be an ounce of gold in your warehouse for every share outstanding. You'll even publish a list of the pieces allocated to the ETF. Your "credits" are unallocated, but easily redeemable, and your ETF shares will be allocated but not as easily redeemable. This differential will buy you the leeway you need to manage your reserves and meet all redemption requests. If someone buys a gold coin from your regular business, or redeems an unallocated "credit" for one, then you will simply deallocate that coin from the ETF, and buy back one share on the public exchange.

"Really clear eyes," as FOA might say, could see that any significant outflow from your ETF was simply you reclaiming the inventory due to a need for it in other parts of your business, and therefore indicative of a scarcity of reserves, even as all purchase and redemption requests were still being met. It reminds me of MF Global and Madoff Investment Securities. Those closest to the companies were the most convinced of plenitude, because all redemptions were being met… until the moment they weren't. The main difference, of course, is that bullion banking is perfectly legal.

This was only a very rough and general analogy to help you visualize GLD and bullion banking in a different way. All characters, businesses, suppliers, customers and funds appearing in this analogy were entirely fictitious. Any resemblance to real characters, businesses, suppliers, customers and funds, living or dead, was purely coincidental.

I agree that, when put this way, it sure sounds sinister, shady and fraudulent, especially to a brainwashed gold bug. But I assure you that everything about GLD is perfecly legal and out in the open. The only reason it seems so darn invisible, is because nobody really understands bullion banking, they picture the way the rest of the gold industry operates when reading the prospectus, etc., and myths built around that view abound. I mean, I think I'm probably the only one in the world who's trying to explain this stuff. As I said above, the coat check concept has been around since GLD was launched, but it's rarely mentioned, and I know why. Even I rarely mention it.

Wimms says I'm doing a disservice to you, my readers, by writing about "coat check". He said I have misguided ideas based on the application of logic to bad assumptions. He said I'm wandering off the path and into the woods. He thinks I have become attached to this coat check idea, and that I'm trying to defend it like dogma.

With all due respect to Wimms, who is, of course, paying me to be here, that's not what I'm doing. I did not write that last post to defend my own personal dogma. Quite the opposite, as usual, I glossed over explaining it because it's a monumental pain in the ass to do so (Q.E.D!). I write about this topic only every two or three years. I wrote about it in early 2011, following the first big drop in phase 2, again in 2013, when the inventory drained for an entire year, and now in 2016, because the inventory is inexplicably rising again. So what I am doing is applying this lens on the rare occasions it becomes relevant, and sharing with you (which is what I do) what I see.

In his first comment, the long one, Wimms linked to a guest post by Catherine Austin Fitts on Zero Hedge. In the summary at the end of that post, Fitts writes this:

"At best, GLD and SLV are simply a bank deposit priced in spot prices without the benefit of government deposit insurance.

At worst, GLD and SLV are vehicles by which investors provide the banking community with the resources to control and manipulate the precious metals market without adequate compensation."

Her "at best" is remarkably close, IMO!

It is true that GLD was not around when Another and FOA were writing, so in that sense I am out on a limb a little with this topic. But it's really not so much about GLD as it is about bullion banking. "Coat check" is about fractional reserve bullion banking, and Another and FOA did write about that. In fact, it is the key to everything they wrote about, and that's why, in my opinion, GLD and coat check matter in the overall scope of my blog.

Again, from Freegold Foundations:

The Free in Freegold

Okay, here it is. What you've been waiting for patiently, I presume. This is what gold will be freed from: The fractional reserve banking practice, which is a carryover from the gold standard.

This is the free in Freegold.

Wimms: "Where does the idea come from that all of London unallocated gold is fractional reserve?"

FOA (1/9/00; 11:22:41MDT - Msg ID:22579)

Comment

This is "gold banking" on a pure fractional reserve basis and very much reflects the dollar prior to 71.

ANOTHER (Fri Dec 12 1997 21:06 - ID#60253)

THOUGHTS!

The paper gold market controlled by the BIS/LBMA system is, alone equal to more than all the gold in existence. This market works like a hybrid currency using approximately twenty to forty percent of all CB gold in leased form as backing. The paper behind the lease is a form of CB/gold and is used as a "fractional reserve" that has built this huge market. This system has worked and does work well. You have but to look at the good value that is received when dollar debt ( digital currency ) is purchased with oil. The world works! But this system cannot continue. There is a limit to how far gold can be inflated in quantity using "fractional reserve leasing" as backing.

Friend of Another (10/14/98; 21:46:26MDT - Msg ID:585)

Tyler Rose (10/14/98; 20:19:54MDT - Msg ID:580)

Using fractional reserve banking, I wonder how many loans could be made with the same million ounces of gold?

FOA (5/15/99; 21:38:42MDT - Msg ID:6212)

Comment on earlier discussion!

It wasn't long before gold was lent without any gold at all! No different than "fractional reserve" banking.

ANOTHER (7/11/99; 17:07:45MDT - Msg ID:8673)

Reply to: USAGOLD (7/10/99; 19:35:16MDT - Msg ID:8634)

Today, the gold sand blows from Central Bank to Central Bank, and is loaned many times. It has become the "fractional reserve" currency that we dare not speak of, but have it we must. The BIS and the ECB now hold the London market in the palm of their hand. And this old British market holds the fate of the dollar in it's hand.

FOA (7/25/99; 22:30:53MDT - Msg ID:9655)

Reply to old question.

This system did make sense as a contracting mechanism alternative from the dollar during a time that they could reasonably self liquidate. But a span of years and commercial speculators through fractional reserve lending has brought yet another quasi-fiat currency (paper gold) to the end of its useful life.

FOA (10/20/99; 19:25:56MDT - Msg ID:17025)

Reply

Like fractional reserve currency inflation, stop the presses and banks fail. Therefore, stop the fractional gold lending and the market "officially" changes!

FOA (10/23/99; 17:01:18MDT - Msg ID:17268)

One long post.

Once the "timeline" of the dollar is near the end of it's mathematical ability to expand world trade, destroy this "new fractional reserve gold market" by adopting "self liquidating rules" into the official sector lending game.

FOA (10/27/99; 6:15:53MDT - Msg ID:17588)

Comment

If everyone wanted their physical gold at once, there isn't enough to cover all the accounts. Official sales and lending will no longer back this "fractional reserve" paper gold market.

Trail Guide (5/25/2000; 14:21:55MT - usagold.com msg#: 31262)

Comment

During this time, the more funds available from investors or fractional reserve banking, the more gold paper is sold, the lower the lease rate, the more paper gold is expanded. Why, almost anyone could borrow gold cash in this fashion.

FOA (09/03/00; 16:27:20MD - usagold.com msg#34)

Of Currency Wars

That's right, this modern world of paper gold very much functions as the same IOUs that currency is based on,,,,,, not much different from fractional reserve dollars.

FOA (10/5/01; 10:55:19MT - usagold.com msg#112)

Discussing the World with Michael Kosares

This is where they must install a free market in gold that ends international confidence in the current gold fractional reserve game.

If anyone would like to read more about the "coat-check room view", I recommend these posts:

http://fofoa.blogspot.com/2013/04/open-window-forum.html

(There's a whole long section on it in this post!)

http://fofoa.blogspot.com/2013/08/my-candid-view-part-7.html

(There's a shorter summary in this post. Just search for "coat".)

And there are two Speakeasy posts from 2013, with slightly different angles:

http://freegoldspeakeasy.com/2013/09/15/another-angle-on-gld/

http://freegoldspeakeasy.com/2013/09/19/another-angle-on-gld-2/

The post preceding this one at the Speakeasy was Plausible Explanations (for GLD’s Recent Behavior), the one following it is Bullion Banking 201, and the current post, from two days ago, is titled LBMA Reserves. If you would like to subscribe, you can do so by clicking here. :D

Sincerely,

FOFOA