Year of the Perfect Storm

______

A perfect storm is an unusual combination of events or things that produce an unusually bad or powerful result.

-Collins

a critical or disastrous situation created by a powerful concurrence of factors. -Merriam-Webster

an extremely bad situation in which many bad things happen at the same time. -Cambridge

a very unpleasant situation involving several bad things.

-Macmillan

a chance or rare combination of individual elements, circumstances, or events that together form a disastrous, catastrophic, or extremely unpleasant problem or difficulty.

-The Free Dictionary

______

In the movie, the doomed vessel faces a confluence of two powerful weather fronts and a hurricane, which the crew underestimates as it races to bring the damaged boat back to port. Then, just as they think there might be hope of making it out alive, a giant rogue wave appears, which overturns the boat and sends it to the bottom of the ocean.

There's a lot happening in the world right now, and it's quite chaotic, so, to keep it organized, I'm going to focus on three storm fronts that I think are converging into the perfect storm, and three waves that I think will converge into a killer wave. They are the dollar storm, the geopolitical storm front, and the domestic political storm front, and then the financial, economic and monetary waves they will create. It's a perfect storm, and it has arrived.

You can read the rest of the post at the Speakeasy, and it's a long one! (See the side bar to subscribe.)

Here I'm giving you two posts from the past six months at the Speakeasy. The first is the fifth installment in my Debtors and Savers series. And the second one is the part of Fourteen which I left out back in August. This first one was posted at the Speakeasy back in July, so enjoy, and have a Happy New Year!

7/25/22

"I want to be clear, though, about one important thing. I’m not an activist. As bad as things may seem, I never advocate activism. I’m an observer and a realist, not a reformer and a dreamer. I advocate preparation for that which is coming. Being aware is being prepared. We don’t win by changing the people on the other side. We aren’t going to change their darkest values. We win because they have gone insane."

-The Debtors and the Savers 2020 Congress of the United States

Washington, DC 20515

An SDR allocation is cost free. Allocating SDRs does not require contributions from donor countries’ budgets. SDRs are a reserve asset, not foreign aid. Most importantly, an SDR allocation does not add to any country’s public debt burden. "Because we are speaking of currencies here, the transition will be brutal!"

-ANOTHER FOFOA's dilemma: When a single medium is used as both store of value and medium of exchange it leads to a conflict between debtors and savers. FOFOA's dilemma holds true for both gold and fiat, the solution being Freegold, which incidentally also resolves Triffin's dilemma. (I should note that the US military is currently at DEFCON 3 due to the war in Ukraine, and will not return to 5 until it's over. It was at DEFCON 5 during most of the Trump administration, occasionally moving to 4 when there was a terrorist threat. It was at DEFCON 4 through most of 2021, and has been at DEFCON 3 through all of 2022. It's possible that the DEFCON system is now under political control, so I just want to clarify that my use of the analogy as it relates to the $IMFS and the brewing internal conflict is totally separate from the current military use of the DEFCON system.) "There is a quote I like that comes from Le Metropole Cafe. It goes, "we will have deflation in everything we own, and inflation in everything we use." This is partly true. It is true during the run up to the rubber band snapping. It is true until we hit the waterfall." You think it’s a problem that the former CIA director thinks half of Americans are literally worse than the jihadi terrorists he routinely killed? In Political Warfare language this is a call to action or a concurrence. This (coming from a General Officer & former Director of CIA is sedition. He is saying average Americans are on par with ISIS. Remember what we did to ISIS? They mean what they say. Unforgivable. https://t.co/2cpY7muN0d pic.twitter.com/Gpv21WrW3L “In our nation’s 246 year history there has never been an individual who is a greater threat to our Republic than Donald Trump.” Dick Cheney pic.twitter.com/erBPBNy8ah Doug Casey: Every country across space and time has the same assortment of people, by character anyway. We have the same kind of people in the US as did the French in 1789 or the Russians in 1917. Our own versions of Robespierre, Napoleon, Lenin, and Trotsky are coming out of the woodwork, and they can see that this is the moment to act. They’re much more interested in power than anything else.

Congresswoman, Stochastic violence. The two classes have less in common culturally, dislike each other more, and embody ways of life more different from one another than did the 19th century’s Northerners and Southerners — nearly all of whom, as Lincoln reminded them, “prayed to the same God.” By contrast, while most Americans pray to the God “who created and doth sustain us,” our ruling class prays to itself as “saviors of the planet” and improvers of humanity. Our classes’ clash is over “whose country” America is, over what way of life will prevail, over who is to defer to whom about what. The gravity of such divisions points us, as it did Lincoln, to Mark’s Gospel: “if a house be divided against itself, that house cannot stand.”

Sooner or later, well or badly, that majority’s demand for representation will be filled. The clash is as sure and momentous as its outcome is unpredictable. for the foreseeable future, American politics will consist of confrontation between what we might call the Country Party and the ruling class. In this clash, the ruling class holds most of the cards The cultural divide between the “educated class” and the rest of the country opened in the interwar years. The reasons for this activity have never been fully explained by the BIS and various conjectures have been made as to why the BIS is facilitating it. One conjecture is that the swaps are a mechanism for the return to central banks of the gold they have secretly supplied to cover shortages in the gold markets.

14! Quite a difference from a few years ago. Recession to borderline depression all but guaranteed in Europe and China, while the US is talking soft landing, LOL. Re-onshoring and near-shoring in full swing with just-in-case more important than just-in-time, super-high dollar probably doing enormous damage to all emerging markets and then some with eurodollar debt, a US that is so split that the other side is considered sub-human as a rule, great local powers re-emerging and the Pax Americana retreating to around US interests only.

A lot has been happening this year! Thanks to your lens, I can take it all in stride. No worries. :-) The freight train seems to have some real speed wobbles now! Imagine a child on a skate board being pulled faster and faster behind a small motor cycle. And then down a small hill. The skateboard's sensitive turning mechanism and small wheels cannot handle the speed, and even the smallest tilt in one direction causes an overcorrection in the other, and an even bigger correction back again. This happens 3 or 4 times almost instantaneously and totally unexpectedly and results in what we used to call a "face plant". Keep in mind that large changes happen at a snail's pace.

The Debtors and the Savers is a conceptual corrective lens for the Marxist view that "the history of all hitherto existing society is the history of class struggle," between the rich capitalists and the poor laborers. The correction goes something like this: The history of all hitherto existing society is the history of monetary struggle, between the easy money camp, those who by nature prefer money to come easy, through printing, borrowing or simply taking it from others, living the easy life off the labor of others, dependent on a system that enables them to disengage from reality, those who I colloquially call the Debtors; and the hard money camp, those who by nature prefer to be independent, self-sufficient, to work hard and earn what they have, take care of their own, and to be left alone, those who I respectfully call the Savers.

The "struggle" is fortunately coming to a head right now. I say "fortunately" simply because the sooner the better. The longer this sucker drags out, the worse the transition will be, and it's already dragged out so long that we're facing a pretty rough transition as it is. I know that some of you don't like it when I say to lie low and sit this one out. I will deal with that issue directly in this post. I will explain why the choice is to sit it out, or be destroyed. But first, let's talk about REPOs, Eurodollars, shadow banking, stablecoins, Tether and system-busting bank runs!

Lev Interview

I listened to a good podcast the other day with a guy named Lev Menand. Lev graduated from college in 2009, and went to work at the Fed. While there, he worked with groups that were tasked with figuring out what happened in 2008, and how to keep it from happening again. Today he is an Associate Professor of Law at Columbia Law School, and he recently wrote a book titled, "The Fed Unbound – Central Banking in a Time of Crisis".

The podcast is 2 hours long, and you can only listen to the first hour at the link. The second hour costs money, and it's in the second hour that he discusses these topics. The first hour is mostly a history of money, central banking and the Fed. So, I'm just going to paraphrase some of his explanations, from memory, and add a few of my own thoughts. I give him full credit, but I may adopt some of these simplified explanations going forward.

First of all, shadow banking is simply nonbanks (1. the REPO market, 2. money market funds) and non-US-banks (3. Eurodollars) that carry dollar-denominated "deposits" for customers (which are generally big companies; the little guy deposits his money in real banks, big players deposit big money in shadow banks). REPOs, Eurodollars and money market funds are all part of the shadow banking system. Tether is a shadow bank. Tether is a stablecoin. The Eurodollar is also a stablecoin (a non-dollar that is pegged to the dollar, and managed to mimic the value of dollar). The financial crisis in 2008 was a bank run on the shadow banking system (a run from non-dollar "dollars" into real dollars). Lehman Brothers was a shadow bank that failed before the Fed and the USG backstopped the whole shadow banking system.

There was another financial crisis in March of 2020 that was also a bank run on the shadow banking system. There was a massive bailout, and no "banks" failed. There was also a pandemic underway, so most people didn't notice the financial crisis, even though the bailout was nominally larger than 2008. In both cases, the nonbank non-dollar "dollars" of the shadow banking system were backstopped with real dollars, but nothing was fixed. There was some reform of money market funds in 2008, but other than that, the shadow banking system still exists as it did before, only now it has the confidence (some would call it the moral hazard) of knowing it's too big to fail.

But is it (too big to fail)? One of the points Lev makes is that no one knows how big it actually is. Not even the Fed knows how many non-dollar "dollars" are out there. He says that's part of the reason they stopped reporting M3, because in reality, they have no idea how much "broad money" exists. In reality, the shadow banking system is likely too big to bail, not too big to fail.

And what the Fed is doing now (hiking rates) shows that it is focused more on its own credibility and high inflation than on financial stability right now. Lev thinks that another "quiet" bank run on the shadow banking system, especially outside of the US (i.e., Eurodollars), could be in the works. Remember, it's a bank run from non-dollar "dollars" into real dollars, which is why the dollar spikes during a run.

His simple explanation of REPOs helps explain how this "bank run" actually happens. The Fed runs its own REPO and RRP markets with the banks, big broker-dealers and money funds, but the shadow banking REPO market is between nonbank broker-dealers and companies with lots of cash to stash. As he puts it, if you're a company with $50 million in cash, you don't go to Bank of America and open an account, you go to a nonbank broker-dealer and put it in the REPO market.

The technicalities of how it works are just that, technicalities. How it works in practice is like making a deposit at a bank, one where you earn a little interest. Only, you can earn more interest depositing at a nonbank than at bank, because a bank has to follow banking regulations, which cost money and eat away at your interest.

Now, as you know, when you deposit your money, even at a real bank, you are essentially loaning your money to the bank. The bank doesn't put your money in a safe, it uses it for other purposes. The same goes for a company depositing $50 million into the REPO market through a nonbank broker-dealer. It is essentially loaning that $50 million to the broker-dealer. But it's not structured as a loan. It's structured as a purchase of a security with an agreement that the security will be repurchased by the broker-dealer the next day (what are called overnight, or O/N REPOs). The security you purchased for a night yields some rate of interest, but you don't get the interest directly from the security. Instead, your share of the interest is worked into the repurchase price of the security. You buy it today at $X, and we'll buy it back from you tomorrow at $X+Y, with Y being your interest rate on the deposit.

Because it's an overnight process, it has to be rolled over each day, and most of the time it is. If you want to withdraw some or all of your money, you simply don't roll it over that day. But remember, just like the bank doesn't keep your dollars in the safe, the REPO broker-dealer doesn't keep your $50 million in cash either. So, if you don't roll it over, the broker-dealer has to sell securities to raise the cash, and not all securities are created equal. Some are harder to sell than others, and if you can't sell enough to raise the cash during a bank run, you go broke. That's what happened to Lehman Brothers.

So, in REPOs, a bank run happens when the "depositors" stop rolling them over en masse. Today, however, the nonbank broker-dealers are probably just Reverse REPOing (RRPing) the cash at the Fed. But not all of it. They will make a bigger spread buying riskier securities with a higher yield than the Fed's RRP rate, which is currently at 1.55% (which is the annualized rate).

That's 155bp (basis points). If you remember, when I wrote about this in July of last year, the Fed had just raised its RRP rate from 0% to 5bp, or 0.05% annualized, on June 21st, 2021. As soon as they did, RRPs almost doubled, jumping from $520B to almost $1T on June 30th, 2021. And that was for a mere 0.05%. Today the Fed's RRPs are at $2.27T (from 101 counterparties, i.e., real banks and shadow banks), earning 1.55%.

Money market funds are a significant contributor to that $2.27T in RRPs as well. In fact, I would guess that it's mostly shadow banks and not real banks in the RRPs at this point. Real banks can't do what shadow banks do due to banking regulations, and they are earning more than the RRP rate on their reserves anyway. The IORB or Interest Rate on Reserve Balances is currently 1.65%, 10bps higher than the RRP rate. I assume that some banks, like the Prime Dealer banks, are required to participate in RRPs to some extent for market making purposes, but with so much shadow bank money in there at this point, that's probably not necessary.

Money market funds are like the REPO market for the little guy. While the REPO market is only available to big money, money market funds give the little guy a way to hold nonbank deposits too, which earn a little more interest than real bank deposits. They do so by creating a mutual fund that buys higher-yielding securities, and the little guy can buy shares in that fund and get a piece of that yield. When he cashes out, he sells his share of the fund. The fund is pegged to the dollar, so it's like Tether, but if too many people cash out at once, it's going to have a hard time raising enough real dollars and holding its peg. That's called "breaking the buck". Money Market Mutual Funds (or MMMFs) are shadow banks for the little guy.

Whether we're talking about the REPO market or money market funds, we're talking about nonbank institutions taking in "deposits" and using them to buy interest-bearing securities, paying a little higher interest than real banks to the depositors, and pocketing the spread between the two interest rates. So, all this shadow bank money that is now going into the Fed's RRPs is pulling that money away from other interest-bearing securities, driving down their prices, and driving up their effective yields. And that puts upward pressure on interest rates across the board (and downward pressure on asset prices).

When I bought my home last November, a 30-year fixed rate mortgage was below 3%, the RRP rate was still 0.05%, and the IORB was 0.15%. 8 months later and the RRP rate is 1.55%, the IORB is 1.65%, a 30-year mortgage is now 6.5%, and it looks like the Fed is going to hike its Fed Funds rate another 75 basis points this week. If so, we could see the RRP rate hiked to 2.3% or higher, and the IORB to 2.4% or so. Just imagine what that's going to do to mortgage rates.

And here's where the "quiet" bank run on the shadow banking system, especially outside the US, might have already begun. No one knows how big the non-US shadow banking system, aka the Eurodollar system, is. And as the value of the securities it holds to back its non-dollar "dollars" gets pushed down, the credibility of its "stablecoin-like peg" to the dollar gets drawn into question. As foreign entities holding large balances of Eurodollars try to move those funds into real dollars, or even just into something else or some other currency, the Eurodollar system is forced to sell securities and buy dollars on the open market, because it doesn't have access to the Fed's discount window or RRPs.

This puts further downward pressure on security prices, upward pressure on interest rates, and keeps driving the dollar higher and higher, making it more and more costly to obtain. And if the Eurodollar's peg was already in question, this makes it worse, in a vicious circle that may be difficult to stop, due to the unknown size of the Eurodollar system, if it really gets going.

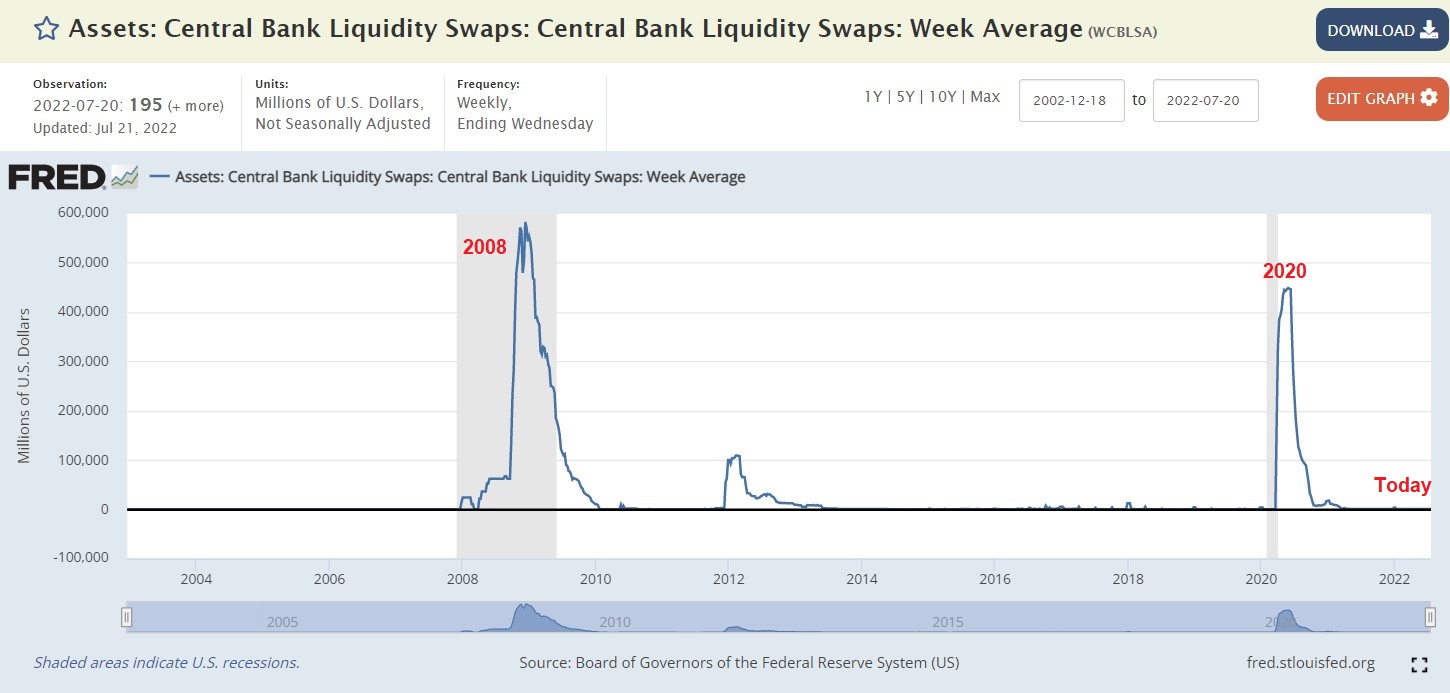

Fed swap lines with foreign CBs backstop the Eurodollar shadow banking system to some extent, but Lev makes the point that the Fed is apparently more concerned with domestic inflation and its own credibility right now than with what's happening abroad. Fed swap lines, which jumped to $583B during the 2008 shadow bank run/financial crisis, held the dollar under 90 at the time. During the March of 2020 financial crisis, they jumped to $447B and held the dollar under 100. Today, they are still at the baseline of $195M with the dollar soaring as high as 108. If there's a financial crisis brewing in the Eurodollar shadow banking system, the Fed is either thus far unaware of it, or doesn't care.

I don't want to put too much emphasis on the Fed and its choices and actions, however, because I don't think they matter that much in the big scheme of things. It's not like if the Fed does one thing, the system will collapse, and if it does another, it won't. When the system is ready to collapse, it will collapse. But understanding what's going on will make it less mysterious when it happens, and then you can explain to all of your friends what just happened, and why you have been buying so much you-know-what for so long. :D

In the end, it will be the USG, not the Fed, that drives the final nail into that coffin. The Fed, as Lev points out, is just a very blunt tool, working with limited information. It just turns on the spigot, and turns it off, then turns it on extra hard when things get bad. Tightening is another story. It's something the Fed is not very good at, though it thinks it should be. It's how the Fed typically fights inflation, however I suspect this inflation, this time, is not about loose monetary policy. It's more about the USG abusing the system.

The $IMFS is quite literally the USG's engine, its power plant. It is what fuels its many branches and bureaus and agencies and departments, and feeds its millions of stooges. And as with any engine, if you abuse it enough, and push it too far, eventually you'll throw a rod, or fuse a piston to the block, or blow it up, or whatever engines do when they die.

Lev understands money and how it works, and so does the Fed for the most part. But the USG most definitely does not. The USG, in case you haven't noticed lately, believes in the Magic Money Tree.

SDR Letter

I want to switch gears here and talk about something a little different, SDRs, and how the Democrats in Congress want the IMF to issue as many as 3 trillion of them, worth nearly $4T in US dollars, and use them to save the poor of the world from debt and COVID. They also want to figure out a way to "recycle" SDRs, circumventing the need for IMF approval, new issuances, and creating what they think will be a "cost-free" Magic Money Tree. This is really just a stunning example of how little the USG understands money, and how it thinks it works. This by itself is not going to end the $IMFS, but the more you know about how things work, and how they were abused in the final stretch, the more you'll be able to impress your friends and neighbors when it all blows up.

The following letter is dated July 12, 2022, less than two weeks ago, and was sent to Joe Biden and Janet Yellen by the Dems in Congress, signed by (among others) deep monetary thinkers like Elizabeth Warren, Corey Booker, Sheila Jackson Lee, Bernie Sanders, Rashida Talib, Ilhan Omar and, of course, AOC. Here's a link to the PDF on the congressional website, but I'm just going to reprint it here for convenience. It's only about 2½ pages:

July 12, 2022

Joseph R. Biden, Jr.

President of the United States of America

The White House

1600 Pennsylvania Avenue NW

Washington, D.C. 20502

The Honorable Janet Yellen

Secretary of the Treasury

U.S. Department of the Treasury

1500 Pennsylvania Avenue NW

Washington, D.C. 20220

Dear Mr. President and Secretary Yellen:

We write to you amid deteriorating economic and humanitarian conditions around the world to request your support, and U.S. leadership, to help developing countries respond to the ongoing fallout of the COVID-19 pandemic, the resulting global economic downturn, and now, the devastating war in Ukraine. We in Congress must quickly approve essential funding toward global vaccination efforts as the Administration has requested in order to address the rise of variants across the world and fight the virus here in the United States. In addition, we urge you to immediately support a new issuance of at least $650 billion in Special Drawing Rights (SDRs) at the International Monetary Fund (IMF) — a simple, rapid, and cost-free way to enable Ukraine, its neighboring allies, and developing countries to respond to, and build back better from, these combined international crises.

The global reverberations of Russia’s illegal invasion of Ukraine are exacerbating an already dire situation for the poorest countries in the world, with global economic growth projected to slow from 6.1 percent to 3.6 percent for this year and 2023.1 As a result of what World Food Programme Executive Director David Beasley called a “perfect storm” of COVID-19, climate disruption, and war, 2 wheat prices have recently hit record highs. 3 Energy and fertilizer prices have also soared, imperiling food production and distribution. 4 The number of people facing acute food insecurity worldwide has already doubled since 2019, 5 and is expected to increase by 8-13 million people this year due to the crisis in Ukraine. 6 As Beasley said in no uncertain terms: “If you think we’ve got hell on earth now, you just get ready,” 7 adding, “Ukraine has only compounded a catastrophe on top of a catastrophe. There is no precedent even close to this since World War II.”8

Developing countries are bearing the brunt of these worsening conditions. Roughly 2.8 billion people — and nearly 85 percent of people in low-income countries — have yet to receive a single dose of a COVID-19 vaccine. 9 Estimated COVID-19 mortality borne by low- and middle-income countries represents 63 percent of COVID-related deaths10 and as much as 86 percent of all excess deaths. 11 UN analysis estimates that if low-income countries’ vaccination rate had been equal to that of high-income countries, their GDP would have increased by $16.27 billion, or 5.16 percentage points in 2021. 12

Furthermore, as a result of the disruption caused by the pandemic and long-existing structural deficiencies in the global financial market, over half of all low-income countries are now in or at high risk of debt distress. 13 In 2020, 62 countries spent more on servicing external debt than on health care; 14 growing indebtedness will likely lead to further reductions in spending on critical needs like health at a time when they are needed the most. Experts warn that, without action, the developing world may soon be plunged into a destabilizing debt crisis. 15 As many as 1.7 billion people in 107 economies may be exposed to this three-dimensional crisis of food, energy and finance. 16

The IMF’s issuance of $650 billion SDRs on August 23, 2021, proved to be a lifeline for low- and middle-income countries. In the six months since, at least 99 developing countries have made use of their allocation — many within weeks of the issuance — to stabilize their currencies, shore up reserves, pay off debts, and finance health care, such as vaccinations, and other urgent needs. 17 IMF Managing Director Kristalina Georgieva estimates that “low income countries are using up to 40 percent of their SDRs on Covid-related priorities, like vaccines and other essential spending.” 18 Nepal, for example, has used the entirety of its allocation, including for financing the purchase of vaccines and other pandemic needs. 19 Ukraine, which was already under severe financial strain prior to the invasion, used the majority of its 2021 allocation, reducing its onerous debt burden. 20 Many more developing countries—including Albania, 21 Benin, 22 The Gambia, 23 Guinea-Bissau, 24 Guyana, 25 Madagascar, 26 North Macedonia, 27 Paraguay, 28 São Tomé and Príncipe, 29 and Uganda30— have all used or committed to using their SDRs to support public health and combat the spread of COVID-19, with Liberia, 31 Pakistan, 32 Senegal, 33 and Sierra Leone34 using SDRs specifically for vaccine imports, production, and distribution.

While vital, this issuance was still insufficient to meet the scale of the crisis. Of the $650 billion that the IMF issued in 2021, roughly $209 billion went to developing countries (excluding China) 35—far short of the $2.5 trillion in emerging market financing needs estimated by the IMF at the beginning of the pandemic. 36 This is why Members of Congress, 37 hundreds of global lawmakers, 38 and development, humanitarian and faithbased organizations from around the world39 have called for an allocation of 2-3 trillion SDRs, and why the House of Representatives approved an allocation of 1.5 trillion SDRs as part of the 2022 State, Foreign Operations, and Related Programs (SFOPs) Appropriations Act. 40

While we strongly support the Administration’s efforts to recycle SDRs held by advanced economies for lower-income countries’ use through Congressional authorization, a new IMF issuance of $650 billion in SDRs is something the Administration can advance right now, under existing authorities. Such an issuance will immediately provide fresh financial resources to help developing economies to meet their critical public health needs, mitigate the humanitarian impact of skyrocketing global food and energy prices, reduce their debt burdens, and respond to and recover from the combined, ongoing crises. It would also be of particular value to the United States and some of its key allies. By boosting demand for U.S. exports, a new allocation has the possibility of creating hundreds of thousands of new American jobs. 41 The Ukrainian government, which called the August 2021 SDR allocation a “great gift for our country,” 42 has used the entirety of its SDR holdings, and Ukrainian Finance Minister Sergii Marchenko has specifically requested access to more SDRs as “a question of the survival of our country.” 43 A new allocation would provide the Ukrainian government with an immediate and vital $2.75 billion boost in its reserves—roughly 2.5 percent of GDP, following an estimated decline by 45 percent this year. 44

Developing countries, and the billions of people who inhabit them, are facing unprecedented challenges and need financial support now. We appreciate Secretary Yellen’s recognition that “we were less successful in supporting poorer countries” during this crisis and “the response to date is not to the scale needed.” 45 As COVID-19 continues to rage, as the reverberations of the war in Ukraine are felt around the world, and as the prospects of an equitable global economic recovery move further out of reach, we applaud her appeal to “ensure the IMF has the tools to fulfill its role of financial firefighter in the face of modern, potentially more frequent, global crises.” 46 In that spirit, we urge the United States to pursue this opportunity to provide cost-free relief worldwide. The United States has demonstrated its leadership and the value of the existing multilateral financial system and we ask that it do so once again. It is currently in the power of the administration to immediately act in support of a new $650 billion new SDR issuance for global relief. We urge you to do so. We thank you for your attention on this important matter.

Sincerely,

Elizabeth Warren et. al.

You can see the rest of the signatures and footnotes on the PDF.

OK, first I want to do a little refresher on what SDRs actually are. SDRs are not a currency. They are not a claim against the IMF as an institution. In fact, the IMF itself holds some SDRs. They are not a loan from the IMF. They are a POTENTIAL claim on any foreign currency, which usually means the US dollar. SDR stands for Special Drawing Rights, so if you have SDRs, you can use them to draw some foreign currency, usually the dollar, which the Fed will print from thin air.

Think of them as kind of like a credit line. As a little guy, say you’ve got a credit card with a limit of $10K that's maxed out. Then your bank raises your limit to $100K. You now have a POTENTIAL claim on an additional $90K, but you don't actually have that $90K in your bank account. SDRs are like that credit line you haven't used yet in that you don't actually have that money in the bank, yet. But they are different in that, once you use them and get the money, you don't have to pay it back.

They are also the unit of account used by the IMF. The value of an SDR is calculated by a basket of foreign currencies: the US dollar, the euro, the yuan, the yen and the UK pound. But there aren't any of those currencies set aside in an IMF "basket" to back the SDR. There is no offsetting purchase of any of those currencies when an SDR is created. And when you use an SDR to draw some foreign currency, you don't get that basket of currencies, you get all one currency, whatever currency you want, which usually means dollars.

SDRs were first introduced in 1969 (and distributed in 1970) as a last-ditch effort to save the Bretton Woods system. The idea was that they would be given free to all members equally, according to their quotas (so not in equal amounts, but proportionally, relative to their size), and they could be used in lieu of dollars or gold in maintaining each currency's fixed exchange rate with the dollar. In essence, they were welfare for weak currencies that were low on reserves.

Since we don't fix exchange rates anymore, today's SDRs are being used as a "cost-free" form of welfare to "low income, emerging market and developing countries," to buy things like vaccines, food and energy, and to pay down their debt. The IMF creates the "cost-free" SDRs out of thin air, hands them out according to quotas, then the poor countries exchange them for dollars from the Fed, which the Fed prints out of thin air, circumventing all other checks on monetary handouts, like monetary policy (QE), budgets, congressional approval, or increasing the national debt. It's voluntary, so the Fed isn't forced to take SDRs from anyone it doesn't like, for example Russia, who is also a member of the IMF and gets its own allocation of SDRs.

I used the term "cost-free" in quotes because it appears in both that letter from Congress, and on the IMF website. Here's what the IMF website says:

Notice the line where they say that SDRs are a reserve asset, not foreign aid. This is entirely untrue today. SDR allocations (to everybody) have only been given out a handful of times. There was the initial allocation of SDR9.3B in 1970, and a second allocation of SDR12.1B in 1979. The next one wasn't until 2009, in response to the GFC in 2008. The 2009 allocation in total was SDR182.9B. And the one after that was the most recent, SDR456.5B, worth $650B in US dollars, given out less than a year ago, on August 23, 2021.

Somewhat ironically, due to the quota system, the countries that receive the most SDRs can't do anything with them, and the poorest countries get the fewest. For example, out of last year's allocation, Germany received 25.5B SDRs, nominally worth US$33.6B, but it can't do anything with them. The US received 79.5B SDRs worth US$105B, and again, there's nothing we can do with them. (They're trying to change that, btw, to make it so we can give them out as foreign aid without the need for a new general allocation from the IMF to everybody. That's what they're talking about in the letter when they say, "we strongly support the Administration’s efforts to recycle SDRs held by advanced Economies…")

Meanwhile, Nepal received 150M SDRs, worth US$197M, the entirety of which was spent on COVID vaccines. And Ukraine received 1.9B SDRs worth US$2.7B, which it had already spent before the war with Russia even began. Reserve asset my ass. As the letter from Congress states, and footnotes, "at least 99 developing countries" cashed in their SDRs within 6 months of receiving them, "many within weeks". That's called foreign aid.

Now, like REPOs, the technicalities of how SDRs work are just that, technicalities. How they work in practice is the unfunded, raw printing of welfare money for poor countries. This money is not borrowed or taxed, it is simply printed by the Fed. That said, I will show you some of the technicalities, so that you can snoop around if you want to, and see what's going on.

The IMF has two departments which keep separate books. One is the General Department, and the other is the SDR Department. The General Department represents the IMF as a distinct entity, while the SDR Department is more like a consolidation of the members. It's similar to the distinction between the ECB and the Eurosystem. The General Department actually holds some SDRs as assets on its balance sheet, currently 22.2B of them worth US$29B, which show up as liabilities on the SDR Department's balance sheet.

When new SDRs are created, everyone receives an asset and a corresponding liability. The asset is called the "holding" or "SDR holding", and the liability is called the "allocation" or "SDR allocation".

So your liability is to the SDR Department, and on the SDR Department's balance sheet it shows up as an asset. Likewise, SDR holdings by members show up as liabilities on that same balance sheet:

Here's Ukraine's financial position in the IMF as of 2/28/22. The link is in footnote 20 on the letter from Congress. Notice that its cumulative allocation (since 1992 when it joined the IMF) is 3.237B SDRs. Those are Ukraine's liabilities to the IMF SDR Department. Its holdings as of 2/28/22 were down to only 13M SDRs:

Here's the breakdown of the 2021 allocation. You can see that Ukraine received 1.928B SDRs worth $2.7B on 8/23/21, and it was down to 13M SDRs worth $17M by 2/28/22. So, Ukraine cashed in $2.687B worth of SDRs in just the last year, and that was before any money it received after the war began.

You might be wondering, why not cash it all in? Why leave $17M on the table? Well, there is an interest rate you pay, in SDRs, when you cash them in:

The SDR interest rate on the date of last year's allocation was 0.05% (incidentally the same as the RRP and 3-month Treasury rates at that time), and 13M SDRs was about 0.5% of Ukraine's allocation, so it was holding back 10 years' worth of interest payments.

As you can see, the interest rate is based on a weighted average of the exchange rates and interest rates of the currencies in the SDR basket, and, of course, both the dollar's exchange rate and interest rates have gone up since then. So if we check the current SDR interest rate, we see that it's now 1.373%:

At that rate, Ukraine's 13M SDRs would only cover about 4½ months of interest rather than 10 years! See how brutal the "strong dollar" can be?

But wait, here's something interesting. Remember that the link to Ukraine's SDR position in the letter from Congress was for 2/28/22? Well, let's see what it is now…

Well, look at that! Somehow Ukraine got another 2.14B SDRs, worth another US$2.8B. That's more than they got last year in the 8/23/21 allocation, and somehow they got it without a new allocation. Notice their liabilities haven't changed. Also notice that they had these new SDRs as of June 30, 2022, and the congressional letter asking for a new allocation was dated almost two weeks later, on July 12, 2022.

Just for fun, I went back and checked Ukraine's position in March, April and May, to see when they got the additional SDRs, and it really jumps around. March 31 – 1,014B SDRs; April 30 – 953.47M SDRs; May 31 – 902.89M SDRs; and now June 30 – 2.153.93 SDRs. It looks to me like someone is giving them mucho SDR-ohs each month and they're cashing them in as they go. So, isn't it interesting that the letter from Congress used the 2/28/22 snapshot in its footnotes, when Ukraine's position was at its lowest, since it was using Ukraine's need for more money as a primary reason for the letter? (Ukraine is mentioned 7 times in the letter.)

This is where you can snoop around if you want to, and try to find more SDR shenanigans. Just use the dropdown menu, and check different countries on different dates:

https://www.imf.org/external/np/fin/tad/exfin1.aspx

You'll find that Russia hasn't cashed in any holdings in the past year. Neither has Iran. Here's the current US position:

Notice that we have 4.28B more SDRs/assets (worth $5.63B but valued at $5.2B on the Fed's balance sheet) than our cumulative allocations/liabilities. That's from raw printing when others redeem their SDRs for cash. It may not seem like much, but it has tripled since last year's allocation. That's 2.833B SDRs we've taken in in the past year, for which we printed about $3.75B, most of which went to Ukraine.

For comparison, the next two in line behind us are China and Japan. Since last year's general allocation, China has taken in 1.9B SDRs (compared to our 2.833B), which means China printed US$2.5B-worth of yuan (compared to our $3.72B). Number three, Japan, took in 742M SDRs, printing about US$975M-worth of yen.

That's a total of about 5.5B SDRs which we know were cashed in for dollars, yuan and yen following last year's allocation. The 15 countries mentioned in the letter from Congress as having cashed in some or all of their SDRs had a combined allocation of 6.07B SDRs. So 5.5B is right in the ballpark. That's a nominal value in dollars of about $7.25B that was printed out of thin air, 52% of which was US dollars, 34.5% Chinese yuan, and 13.5% Japanese yen. Of the roughly $3.75B US dollars we printed, at least 70% went to Ukraine.

Again, I realize that this doesn't sound like a very large number in today's world, but this use of SDRs as a form of raw printing for foreign aid is a fairly new thing. And this gives us a glimpse at the scope of it. From a US$650B allocation of new SDRs (more than twice the number of all previously-issued SDRs combined), about US$7.25B-worth of new cash gets printed out of thin air, with no debt, asset purchases or taxation backing it up. Pure global MMT.

That's a printing rate of about 1.1%, and the Dems would like the IMF to issue another $4T-worth of SDRs, according to that letter, to help the entire world get vaxxed and out of debt. At 1.1%, that would mean about US$44B printed. But that's not enough. That's not what they want. They want US$2.5T-US$3T printed for global welfare, which translates to about 273T SDRs. See how math can be fun? :D

And to the former gold writer who wishes not to be named, who brought this to my attention, I finally solved the mystery of the missing SDRs. It's so simple it's almost embarrassing.

He asked me if central banks carry SDRs as assets in a greater quantity than the IMF carries them as liabilities. He wrote: I don't see the 650 bil or so SDR liabilities in their BS:

The answer is in the date of the snapshot taken on that statement. It's dated April 30, 2021, and the last allocation didn't happen until August 23, 2021.

So we take the 660.7B total SDRs as of today, subtract the 8/23/21 allocation of 456.5B, and we get 204.2B total SDRs as of 4/30/21. And if we add up the total allocations from the SDR Dept. BS…

For clarity, 111.895B was the total allocation to all countries who had cashed in some SDRs as of 4/30/21, and therefore had fewer SDR holdings than their allocation. And 92.302B was the total allocation to all countries who had bought SDRs from other countries, and therefore held more SDRs than their allocation.

These numbers show that of all SDRs used, i.e., actually exchanged for foreign currency, in its entire 52-year history, 15% happened in the last 11 months. Like I said, this idea of issuing new SDRs as "cost-free" foreign aid is a fairly new thing, and the Dems in Congress just got wind of it.

YOTC

I wrote the first Debtors and Savers post in July of 2010, twelve years ago this month. The second one was two years later, in 2012. Then it was four years until the third one in 2016, and another four years until the fourth one in 2020. This is the fifth in the series, and I'll note that it is coming only two years after the fourth. It kind of feels like I have come full circle: 2-4-4-2. Things slowed down for a while, now they are moving fast.

In hindsight, things are much clearer than through a crystal ball. The first Debtors and Savers featured Karl Marx and his prediction of the breakdown of capitalism as a result of class struggle, basically between the owners and the workers. Turns out it's just the Marxists, undermining society to destroy it.

The second one featured a self-described Marixst named Ash, who liked to attack me on another blog, writing a series of five or six posts purporting to debunk Freegold using Marxist concepts. He also wrote a post called The Orkin Man, which I characterized in 2012 as a "batshit-crazy worldview." The idea in The Orkin Man was that people like "Uncle Joe" Stalin, Mao and Pol Pot were the Orkin Man of their time, purging (by killing) their "class enemies" from society, and that we need to find an Orkin Man for today. "Who gets to be the Orkin man?", he wrote. "What is rotten must be removed." At the time, I thought it was a fringe, extremist view. I have since learned that it is more common than you can imagine. If you ever wondered how leftists can look back fondly on the French and Communist Revolutions, this is how.

The third D&S was inspired by Trump winning the Republican primaries, which I saw as a repudiation of Progressivism, or Cultural Marxism, which I thought had peaked with absurdities such as Bruce Jenner, dressed as a woman, gracing the cover of Vanity Fair, and laws allowing men dressed as women to use women's public restrooms and locker rooms. Trump won alright, but things just kept getting more and more insane.

The fourth one was in July of 2020, almost two months into the George Floyd riots, and 3½ months out from the election. I didn't pretend to know who was going to win, but I knew that whichever way it went, things were going to get ugly. I wrote in my New Years post that year, "Something big is going to happen this year. I know this for a fact, because, at the very least we have another presidential election this year, on Nov. 3rd. And either Trump will be reelected, or someone else will be elected, and either way, half of the country will be very unhappy with the result."

Even though I didn't know who was going to win (because I knew the other side was going to cheat), there was one thing I was pretty sure about. I was pretty sure that Joe Biden wouldn't be the candidate. He was the presumptive nominee at that point, but I was pretty sure they were going to nominate someone else at their upcoming convention. I did get one thing right, though. In D&S2020 I wrote, "If Biden (or whoever the Democrat candidate is on Nov. 3rd) wins, then the revolution is on and it’s open season on the Right."

I was wrong about Biden, though, because I was missing a crucial piece of information that I would only learn after the election. They never wavered on pushing Biden through because they had a secret weapon, a failsafe, an ace in the hole. It's like a turbo booster on their election machine. I don't think they wanted to use it, because they didn't use it until something like 4AM, the morning after the election, but they knew they had it in their back pocket if they needed it. It's what looks like this when graphed:

By 7:15PM (10:15PM Eastern), Florida had been called for Trump, British betting markets had flipped to Trump winning, and Trump was leading the popular vote by 1.7M, which was significant that early. It wasn't going to be the landslide that some had hoped for, but it was a good bet at that point that Trump was the winner, so I decided to do the livestream. In terms of that graph, we were livestreaming this whole time, so we were awake all night, and some of us watched them push that turbo button in real time:

The turbo button probably wasn't available in 2016, at least not at the scale of a national US election, or they probably would have used it then. I think it's something new, at least at this scale, and that's why they didn't really want to use it. It was risky to use at this scale, because it risked exposing the whole project. And it did expose it, because we're talking about it now. So far they've skated, but the truth is out there and they know it. So I don't think they dare use it as boldly this year as they did in 2020. They can't risk it this soon. Their secret weapon is no longer a secret, so too many people will be watching too closely. The risk is too high right now, so they won't have their ace in the hole this time.

Probably the most important takeaway from what I've learned since the 2020 election is that elections are their Achilles' heel, and they know it. And, because they know it, they will always protect it at all costs. But they also have a second Achilles' heel which they don't know about, and that's what will bring them down. More on that in a moment, but first let's talk about elections.

Did they cheat in 2008 and 2012? Well, let's just say that earlier versions of their election machine were in operation at those times. 2016, however, caught them off guard. They thought they had 2016 all sewn up. Remember all the polls giving Hillary a 99% chance of winning, right up to election day? That's because they thought the fix was in. But Trump simply got too many votes, so they had to give up the White House for a while. Luckily (for them) they had enough allies (and corrupt or compromised opponents) inside the government to prevent a full transfer of power, and they set out to take it all back in the next presidential election.

Then, again in 2020, they thought they had it all sewn up, but once again, Trump got too many votes, and they had to use the failsafe turbo booster button. The extra vote injection took them over the top, but at the cost of exposing the machine they’d spent two decades refining. Granted, it’s still operational (it hasn’t been dismantled, yet), but it has been exposed.

So, elections are now their biggest problem. They won the last one, barely. They didn't win fairly, but they did win, and they now control the US federal government, and all of its departments, agencies and bureaus. That's a whole lot of power that they control, and they know it. And they are currently using it and abusing it, no holds barred. As ByiamBYoung noted, it's depressing to watch.

But elections are now their biggest problem, their weakest link in the chain of time, and there's another one coming up in a little more than 3 months. They can’t win this November in a fair election, and they can’t rig it either, at least not to the extent that the outcome is certain. Same goes for 2024.

From their perspective (put yourself in their shoes), they need certainty for the 2024 election. They’re not going to just lose in 2024 and hand the power back, they’re in too deep. It’s existential for them now. There are too many skeletons in too many closets that they can’t let anyone anywhere near the closets. It’s all or nothing for them now. But if they lose ground this year, it will make securing the outcome in 2024 much less certain, and riskier for each of them individually.

That’s why I think they want to make a move this year, before November.

That's why I named it YOTC. If it doesn't happen before the election, then something is likely to happen right after, likely before the end of the year. I can't say specifically what that thing is, but it has to do with nullifying the MAGA vote. There's no North and South like there was in 1861, so it's not like that.

They don't need an all-out conflict with the right. They couldn't win that anyway. They just need to crush anyone who gets out of line, and declare anyone who doesn't support the outcome of the 2020 election a domestic terrorist. The game is to suppress the MAGA vote in that way, but it will fail in the end because their power plant (the $IMFS) will fail in the process.

That's their other Achilles' heel, the one they don't understand. The one they won't protect, but will instead abuse to the nth degree (which they already are), eventually throwing a rod, fusing a piston, or simply blowing it up.

Even with all that they control in the federal government, they don't have enough forces to come after everybody. So they'll only come after those who aren't lying low. Those who stick their necks out will get their heads chopped off. Those who make a stand will be crushed. They simply have too much power right now. We can't win this one by fighting back. But when they can't pay their forces anymore, it'll end.

Sitting this one out simply means staying on defense while they have all the power, because sooner or later they are going to shoot themselves in the foot, the one with the other Achilles' heel. :D

They are going above and beyond full retard right now, not just because they actually are above and beyond, but also to delegitimize the USG in the eyes of millions on the right, in hopes that there will be some civil disobedience, or worse. Then they will come in and crush those who disobeyed. That's the game right now, and it could easily escalate. Activist disobedience is foolish right now, but defensive disobedience is necessary. Don't be the fool. Make it to the other side.

COVID, The Jab, Monkeypox, J6 Hearings, Ukraine, and Everything Else

I know that there have been lots of twists and turns over the past few years, so many that it can feel overwhelming. But just because you didn't see them coming, doesn't mean they changed where the river ends. It ends with the brutal transition to a new monetary system, one not based on the US dollar.

That hasn't changed. The European central bankers knew it in Belgrade in 1979, they knew it in 1988, it's what ANOTHER wrote about in 1997, it's what I've been writing about since 2008, and it's still true today.

Also, gold will not be part of the new monetary system like it is today, trading as just another currency on the FOREX. It will be set free (i.e., Freegold), because bullion banking will not survive the transition. Bullion banking is like a shadow banking system for physical gold, and like the dollar shadow banking system, it will experience a run. But unlike the dollar shadow banks, there will be no one to bail it out. It's like a stablecoin, pegged to the physical market, and like Tether, sooner or later it will end.

ByiamBYoung's comment really drove home how overwhelming all of these other things can seem, but don't let them distract you from what you have always known, at least since you've been here. It hasn't changed. Subjectively, perhaps you had some unrealistic (in hindsight) expectations, or biased perceptions, but objectively it hasn't changed.

The debtors are in charge. They won the election. They have all the power right now, and lots of it. Arguably (of course), they can be blamed for all of those depressing distractions. The savers, meanwhile, are hunkering down, falling back, and preparing for what is coming, knowing that the debtors' engine, their power source, cannot run without fuel, oil and upkeep. They watch, as the debtors rev that engine like it's a Tesla running on magic electrons that come from magic electron trees. They lie low and wait, knowing that soon it will catch fire, and being so disengaged from reality, they won't have a clue what to do about it. We wait.

Sincerely,

FOFOA

Back in August, I posted the beginning and the end of my 14th anniversary post from the Speakeasy, but I left out the middle portion which was about 80% of the post. I'm not posting the beginning again here because it is unnecessary, but you may want to go read it again. Here's the link:

http://fofoa.blogspot.com/2022/08/fourteen.html

And here, we pick it up where I left off:

Let's start by clarifying the DEFCON analogy, since DEFCON 4 might not seem very serious when DEFCON 1 is the highest. First, we have never been at DEFCON 1. The military term for DEFCON 1 is "Cocked Pistol." It's the "This is it, it is now" moment, to quote someone named Jim. On a global basis, in fact, the US military has never been higher than DEFCON 3.

The most famous example of a DEFCON 3 is immediately following the 9/11 attacks, then it was lowered back to DEFCON 4 three days later. The most famous example of a DEFCON 2 is the Cuban Missile Crisis in 1962, when the Strategic Air Command was raised to DEFCON 2 for 22 days, while the rest of the military remained at DEFCON 3. Again, the US military as a whole has never been above DEFCON 3.

So, the jump from DEFCON 4 to DEFCON 3 is a really big deal. The Danger Zone is DEFCON 4. In my terms, we are now at DEFCON 4, with a good chance of moving to DEFCON 3 before the end of the year. If not by the end of the year, then before 2025 for sure, with the probability rising with each day that passes. And in any case, we don't return to DEFCON 5 until it's over. That's what's different about this year from past years.

I called a Danger Zone on 9/17/19, the day the overnight REPO rate spiked to 10%. That post ended with the line (from Nosh), "The smell of Lehman is in the air." Then on 10/9/19, I wrote, "The danger zone continues." And on 1/22/20, I wrote, "Hang on tight, because we’re still very much there. We’re still very much stuck in the danger zone, as far as the eye can see."

Less than two months later, we had a financial crisis, a run on the shadow banking system that was nominally larger than 2008, but hardly anyone noticed, because A) there was no Lehman moment, and B) COVID. That was followed by bailouts, lockdowns, riots, massive cash giveaways and the 2020 election, and somehow the $IMFS survived.

2020 was full of surprises that no one saw coming. It was the epitome of the Danger Zone, and yet we seemingly returned to DEFCON 5. It's certainly debatable whether we ever actually returned to DEFCON 5 or not, and I did say that we were stuck in the Danger Zone "as far as the eye can see," but I think we have crossed that horizon, and can now see the end.

So, while we may very well have been stuck at DEFCON 4 since 9/17/19, there are two main differences between then and now. In 2019, nobody could have seen what 2020 would bring, at least not all of it, but now I can see what's coming. Also, while the Danger Zone was an easy call that day in Sept. of 2019, no one could have taken it as far as I can today, and make the call that we'll be at DEFCON 4 until we move to DEFCON 3, without ever returning to DEFCON 5 before the end.

The basis for my call is that the $IMFS can't survive the conflict, and the conflict is simply unavoidable. I don't say that as an advocate for conflict, but as a passive observer who has run countless scenarios in my mind, calling it as I see it, and preparing for the worst while hoping for the best. The best and worst, however, are merely different possible variations of the $IMFS-ending conflict.

If you don't get the concept of the conflict that I outlined in my New Year's post, and I know some of you don't (especially those outside of the US), then I'm afraid I can't explain it to you. You'll just have to write this one off under #KFW, and if you don't know what that means, just ask. I'm sure someone will tell you.

And that doesn't mean that I know what the proximate cause of the collapse of the $IMFS will be. There are plenty of wildcards out there that could pop this sucker even before the conflict finishes it off. Russia and China are openly talking about their desire and plans to break the dollar system and the LBMA. Our own government is openly abusing its own currency. The Fed is (wittingly or unwittingly, doesn't really matter) playing with fire, and there's something going on with Eurodollar liquidity right now which I haven't quite figured out.

The point is, there are plenty of technical hurdles the dollar must navigate just to keep moving, as there usually are. And there's always some probability or likelihood that one or more of them will take it out, although so far it has proven to be more robust than expected. But now we have this internal conflict brewing inside the US, concurrent with and inextricably linked to a supply/demand-driven inflation/deflation conflagration that will, in the end, destroy the $IMFS.

I have long discussed US dollar hyperinflation in simplistic and theoretical terms. But now that I see it unfolding in the real world, it's a bit more complicated, as you'd expect.

First, we already have serious price inflation in necessities like food, shelter and energy, and for most people, that means a shortage of money to spend on anything else. In the case of food and energy, it is supply-driven inflation, meaning it's not people consuming more food and energy that's driving up prices, it's that there's not enough food and energy to supply what people are used to consuming.

For shelter, the housing market, it's demand-driven inflation, meaning too much easy money and easy credit chasing real estate for profit rather than shelter. It is a bubble, and it is currently slowing down. The higher end of the market has more staying power than the lower end, but the higher end pulls the lower end up in price even as sales drop off a cliff. The real pain, however, is felt by the renters, as rents rise to match the bubble prices.

In the US, 1 in 3 households rent their home. That's 44 million households out of a total of 123 million households. If you want to see some real anger, go find a local Facebook marketplace group, where people occasionally advertise their investment homes for rent. Find one that allows comments under each listing, and read the comments complaining about rental prices now versus even just a year ago. Renters are mad as hell right now, and don't forget these landlord memes from D&S2020:

Target is just one example, but it's a good one because, like the price inflation in necessities, it happened this year. This past quarter, Target "was forced to slash prices to clear unwanted inventories of clothing, home goods and electronics… warned that it was canceling orders from suppliers and aggressively cutting prices because of a pronounced spending shift by Americans as inflation cuts into spending on non-essential items."

So, right now we have price inflation in essential goods, and price deflation in non-essentials. Something that goes hand-in-hand with price inflation and deflation is shortages and gluts. Shortages in essential items, and gluts of non-essential items. This is an expected step on the run-up to full-blown hyperinflation, which I wrote about as early as 2009, in a post called The Waterfall Effect:

Meanwhile, the Fed is purportedly trying to fight supply-driven price inflation in essentials by killing demand. It is pulling money (i.e., "demand") out of the money supply by shrinking its balance sheet and raising interest rates. This is monetary deflation, and it is more likely to cause asset deflation in things like the stock, bond and housing markets than to help those who can barely afford the essentials. In fact, it will make things like food shortages even worse, by killing the economy that keeps store shelves stocked. Some even think that's the goal, an "active measure" in the brewing conflict, or at least that the Fed is doing the bidding of the administration.

In any case, there are multiple vicious circles at work right now, so it's going to get much worse before it gets better. The administration is working overtime to conceal inflation in ways that will only make it worse. So don't think that anything is being fixed. It's going to break before it gets fixed. You can't fix it, all you can do is prepare.

These two videos are kind of a side bar. They were something I just stumbled across while doing an image search for "empty shelves hyperinflation", and I thought they were worth sharing (even though they have few views and come from a small account with only 572 subscribers which hasn't made a video since January). I thought they might spark a useful discussion in the comments, and I pretty much agree with all of the points he makes in this next one.

I know they are not all practical for most people, like paying off all debt, or moving out to the country and raising chickens. But I think it's at least worth thinking about why they might be good ideas for some people, even if they don't work for you. The idea with debt is that, as the prices of essentials keep rising and eventually skyrocket, debt service may become a stressful burden, and the stress may cause some people to make mistakes at exactly the wrong time. What I did with some debt, personally, was I took advantage of my recent move to consolidate what little debt I had into a 30-year fixed rate loan with a small local bank, which I hope to pay off with revalued gold.

It's a small percentage of my overall position, which I could pay off if I sold some gold, but the consolidation brought a meaningful reduction to my monthly expenses, as did the move itself. Even so, I am still starting to feel the pinch of inflation at this point.

Regarding the video, I should mention that I know some of you are making the hyperinflation debt play. And while I hope it works out, I have never advocated it as a play because I don't think it's a sure thing. As long as you have enough income to comfortably carry the debt, it's a fair gamble. Theoretically, your nominal debt will get hyperinflated away and you'll be able to pay it off with a few small coins. I get that as well as anyone, but I'm not making that play. I'm fine with just the coins, and as little debt as possible, for convenience. I'm trying to keep it as simple as possible.

OK, so, getting back to why we're not returning to normal (DEFCON 5) before the end (the transition we've all been waiting and preparing for), what guarantees this outcome is the US system of national elections. We have regularly-scheduled national elections every two years, and a presidential election every fourth year. You could do a countdown timer, because they're hard and fast dates. I'd do one, but they changed a few things on WP and it's not as simple as it used to be. Anyway, there are now 77 days left until the midterm elections, and 805 days until the presidential election in 2024.

There are two bitterly-divided sides in the US today, and neither one is backing down. There is no middle ground. It's a different situation than in other places around the world, for many reasons. And the divide is more complicated than you think. If you think you understand it completely, then I guarantee that you don't.

This next presidential election, in 805 days from now, is not just another election. The last two presidential elections, in 2016 and 2020, were extraordinary events, each in their own right. And together they set the stage for this next one, which is going to be ultra-extraordinary. There really aren't words to describe the magnitude of what I'm trying to say, so I'll just leave it at that.

One side has all the power right now, and the other side has more than enough people to win even a moderately-fair election. By the way, the two sides are not the Republicans and the Democrats, or the conservatives and the liberals, or even the Left and the Right. It's a little more complicated than that. More on that in a moment.

Now, I know what some of you are thinking (hi BF and Matrix! :D). You're thinking that the sheep are never going to wake up and take back their country. You're frustrated at how passive the Right, or MAGA, or whatever we want to call them for convenience, are. And I agree! We (I'll include myself in this group) are not activists. The other side are the activists. Always have been. They want to cause change, we want to preserve, or conserve. We are passive or reactionary, but one thing we are good at is getting out the vote (without the need for get-out-the-vote ad campaigns).

This is a problem for the other side, the side that has all the power right now. It's a problem because of the US system of regularly-scheduled national elections. The last two elections were so extraordinary because the first one shocked the hell out of the other side (they DID NOT see THAT coming), and the second one shocked the hell out of our side (I say "our side" because I think most here are on the same side, while acknowledging that I know a few of you are not).

As the midterms approach, the side with all the power is showing its hand. While our side is showing strength at the polls, which is what we do, the other side has made it clear that they will use and abuse the massive power that they control to crush and delegitimize the other side.

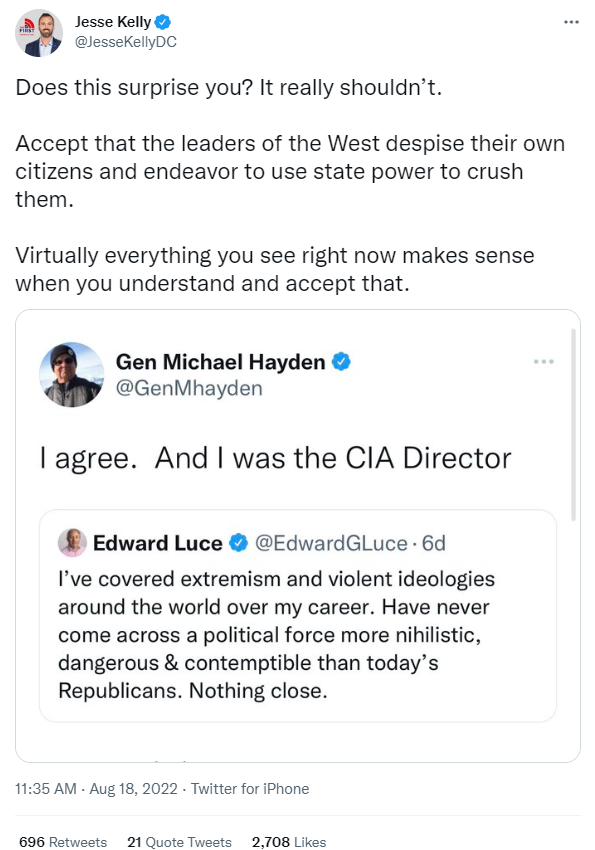

That's what the tweet above is about. Michael Hayden was a four-star general in the Air Force, and he was director of the NSA, the DNI and the CIA, all under a Republican administration during the first eight years of the War on Terror. And he's saying, quite clearly, that MAGA is more dangerous than ISIS.

If you think the most powerful people in the country don’t want to kill you, you’ve got no idea what’s going on. pic.twitter.com/Bjklm9FRkI

Here is Dick Cheney, the (Republican) VP during that same time period, saying that in our nation's 246-year history, there has never been an individual who is a greater threat to the country than Donald Trump:

— ★ 𝔸𝕝 𝔾𝕠𝕣𝕓𝕒𝕔𝕙𝕖𝕧 ★ (@RealAlGorbachev) August 4, 2022

Oops, wrong one. Here you go:

These are two people who held office at the highest levels of government during the War on Terror, now saying that Trump and the 70 million Americans who voted for him are a greater threat. But it's not just them. There are plenty more of lesser stature and on the Dem side of the aisle saying worse things about their political opponents. This is political warfare. We're showing up to vote, and they're waging political warfare.

Someone sent me a Doug Casey interview the other day, and there was a piece I wanted to quote from it:

Our own versions of those types are coming to the fore. The average American is confused and rolling over—he doesn’t have any philosophy or ideology to counter them. So, we could have a variation of what happened in France or Russia.

There is a new term I've come across recently (at least new to me). It's stochastic violence. It's the idea that if you inflame enough people with inflammatory rhetoric, there is a statistical probability that someone will eventually snap and resort to violence. If you look it up on Twitter, it's almost entirely people on the left using the term against the right as a means of silencing, for example, criticism of sex-change medical procedures on kids. Here's an example:

Please get FBI involved, as well as whatever you can do with social media companies to remove those responsible for inciting violence. The longer this goes on, it becomes inevitable that stochastic violence will occur. Cut it off at the pass.

But to me this looks like projection, because the inflammatory rhetoric seems to be coming mostly from the left, directed at Trump supporters in particular, calling them domestic terrorists. Stochastically, it serves to incite leftist mob violence (riots) against those being labeled as domestic terrorists, it may push some Trump supporter(s) into doing something really stupid, and it also gins up public support for more mass prosecutions and gulag-like imprisonment like we saw with J6.

This Trump-supporters-as-domestic-terrorists narrative is being amplified at scale right now, if you know where to look. So, statistically there is a good chance of someone snapping, or something happening. And whatever it is, to make sure it gets blamed on Trump supporters, there are thousands of people right now, Feds, other law enforcement, the Lincoln Project and other leftist busybodies, documenting everything everyone says.

If you're on the right, and you simply say "look at what they're saying and doing, this isn't going to end well," that right there is inciting violence. It's what they are calling stochastic violence. It's how they equate words with violence, and even just pointing out the obvious, or in some cases simply making a joke, is now stochastic violence, and must therefore be silenced. I know it sounds crazy if you haven't seen it for yourself, so here's another example:

To be fair, I don't know for sure that this person is referring to Tucker Carlson's report itself as stochastic violence, because it's possible he's referring to the violence in Tucker's report. So here's one more example:

Now that's some funny stuff, but it's certainly not inciting violence. [Unfortunately, the ad is gone. He was holding a rifle saying he was going RINO hunting or something like that.] He's talking about voting RINOs (Republicans In Name Only) out of office. It's what's happening right now in the primaries, and no one is going to mistake that ad as a call for violence. Even stochastically it's nil, unlike labeling half the country as domestic terrorists, and threatening to come at them with the full force of the federal government, the DOJ, IRS and FBI. If anything is stochastic violence, it's that.

So, who are all these potential domestic terrorists? Well, let's just call them the Country Class.

Three weeks ago, Lisa posted a good article by Michael Anton, titled They Can't Let Him Back In. In it, he referenced an article by Angelo Codevilla, titled America's Ruling Class (And the perils of revolution), writing: "Anti-Trump hysteria is in the final analysis not about Trump. The regime can’t allow Trump to be president not because of who he is (although that grates), but because of who his followers are. That class—Angelo Codevilla’s “country class”—must not be allowed representation by candidates who might implement their preferences, which also, and above all, must not be allowed."

In The Debtors and the Savers, I did not dispute Marx's assertion that history is the story of class struggle between two classes. What I disputed was his delineation of the two classes. Marx says it's basically the rich and the poor, while I said it was the "easy money camp" (the "Debtors") and the "hard money camp" (the "Savers"). Angelo Codevilla calls the two classes the "Ruling Class" and the "Country Class." I really liked his description of the Country Class, and I think his delineation of the classes is completely compatible with mine. It's a long article, so here are a few snippets. BTW, this was written in 2010!

The Political Divide

Important as they are, our political divisions are the iceberg’s tip. When pollsters ask the American people whether they are likely to vote Republican or Democrat in the next presidential election, Republicans win growing pluralities. But whenever pollsters add the preferences “undecided,” “none of the above,” or “tea party,” these win handily, the Democrats come in second, and the Republicans trail far behind.

[…]

In short, the ruling class has a party, the Democrats. But some two-thirds of Americans — a few Democratic voters, most Republican voters, and all independents — lack a vehicle in electoral politics.

Sooner or later, well or badly, that majority’s demand for representation will be filled.

[…]

Far from speculating how the political confrontation might develop between America’s regime class — relatively few people supported by no more than one-third of Americans — and a country class comprising two-thirds of the country, our task here is to understand the divisions that underlie that confrontation’s unpredictable future.

[…]

What sets our ruling class apart from the rest of us?

[…]

Wealth? The heads of the class do live in our big cities’ priciest enclaves and suburbs, from Montgomery County, Maryland, to Palo Alto, California, to Boston’s Beacon Hill as well as in opulent university towns from Princeton to Boulder. But they are no wealthier than many Texas oilmen or California farmers, or than neighbors with whom they do not associate — just as the social science and humanities class that rules universities seldom associates with physicians and physicists. Rather, regardless of where they live, their social-intellectual circle includes people in the lucrative “nonprofit” and “philanthropic” sectors and public policy. What really distinguishes these privileged people demographically is that, whether in government power directly or as officers in companies, their careers and fortunes depend on government. They vote Democrat more consistently than those who live on any of America’s Dr. Martin Luther King Jr. Streets. These socioeconomic opposites draw their money and orientation from the same sources as the millions of teachers, consultants, and government employees in the middle ranks who aspire to be the former and identify morally with what they suppose to be the latter’s grievances.

Professional prominence or position will not secure a place in the class any more than mere money. In fact, it is possible to be an official of a major corporation or a member of the U.S. Supreme Court (just ask Justice Clarence Thomas), or even president (Ronald Reagan), and not be taken seriously by the ruling class.

[…]

Since the 1970s, it has been virtually impossible to flunk out of American colleges. And it is an open secret that “the best” colleges require the least work and give out the highest grade point averages. No, our ruling class recruits and renews itself not through meritocracy but rather by taking into itself people whose most prominent feature is their commitment to fit in. The most successful neither write books and papers that stand up to criticism nor release their academic records. Thus does our ruling class stunt itself through negative selection. But the more it has dumbed itself down, the more it has defined itself by the presumption of intellectual superiority.

[…]

Its first tenet is that “we” are the best and brightest while the rest of Americans are retrograde, racist, and dysfunctional unless properly constrained.

[…]

The cultural divide between the “educated class” and the rest of the country opened in the interwar years. Some Progressives joined the “vanguard of the proletariat,” the Communist Party. Many more were deeply sympathetic to Soviet Russia, as they were to Fascist Italy and Nazi Germany. Not just the Nation, but also the New York Times and National Geographic found much to be imitated in these regimes because they promised energetically to transcend their peoples’ ways and to build “the new man.” Above all, our educated class was bitter about America.

[…]

…the notion that the common people’s words are, like grunts, mere signs of pain, pleasure, and frustration, is now axiomatic among our ruling class. They absorbed it osmotically, second — or thirdhand, from their education and from companions.

[…]